Anatomy of a top VC: 397% IRRs and 17-IPO funds

Richard Murphey

In this post, I’ll analyze some of the top venture funds of the last decade: what financial returns did they generate, what kinds of companies did they invest in, and how did they structure their portfolios.

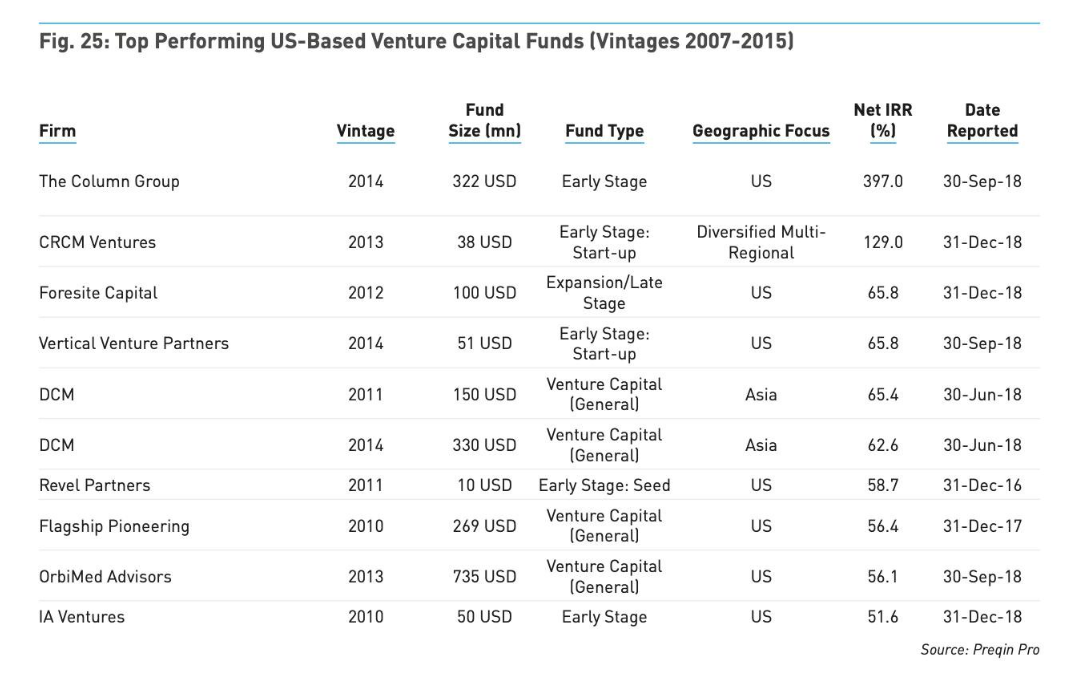

In particular, I’ll look at funds from this list of top-performing VCs provided by Preqin. I’ll focus on funds with at least $100M in assets, as it is harder to generate high returns with larger funds, and only look at US-focused funds, as I have more data on the US venture industry than VC in other countries. So the funds I’ll analyze are The Column Group, Orbimed, Flagship and Foresite.

Besides being large, top-performing, US-focused venture funds, what else do these funds have in common?

They only invest in biotech.

Specifically, biopharma – FDA-regulated prescription drugs.

Biopharma is the second-largest sector of the VC world after software, having attracted $17B in VC funding in 2018, but has traditionally been viewed as uninvestable by most VCs. How, then, did these biopharma VCs outperform the rest of the industry?

Before jumping in, it is important to note that this list of top performing VCs is not comprehensive. It only includes funds that self-report returns or that have LPs that publish returns. There may be some large tech funds that would make this list, but we don’t know, as we don’t have the data. If you have any corrections, please let me know!

Investment strategy is about more than picking winners

In another post, I show that the best-performing biotech startups generate lower returns than the best-performing tech startups (though not by as much as you might think). If that’s the case, then how do biotech funds outperform tech funds?

As we will see below, the answer is that investment strategy is not just about picking winners, but about managing risk across a portfolio. These biotech funds are quite concentrated, invest at low valuations, and have low loss rates. This contrasts with the “power law” strategy practiced by many software VCs, where the only important thing is investing in a few really big companies – if you do that, it doesn’t matter what valuation you invest at, or how many other investments lose money.

Analyzing the portfolios

My sources for these analyses are press releases and SEC filings. These sources don’t have enough data to get to the IRRs posted in the above chart, although we can get a reasonable but imperfect sense of the cash-on-cash returns.

This analysis, while informative, suffers from some limitations because it is limited to publicly available information. The most significant limitations are:

- My estimated returns for companies that exit through M&A while private are very rough, as there is limited public data on the amount that VCs owned in these companies. Further, many of these M&A deals include milestone payments as consideration, and I do not know whether the milestones have been achieved. Fortunately there are fewer of these in biotech than tech, as the IPO window for biopharma startups is wide open.

- The list of companies funded by each fund is not comprehensive. If a fund does not publicly disclose its investment in a startup, then it won’t be captured here.

- It is not possible to calculate IRR for these funds. I don’t have data on the amount invested per fund for companies that didn’t go public. Even companies that did go public don’t always disclose amount invested per investor in all of their venture rounds. Further, I don’t have exact data on the timing of investments.

- I do not know when / if each fund has exited its public investments.

The Column Group

The Column Group (TCG) is, in many ways, different from your typical VC: they focus exclusively on biopharma, they create most portfolio companies in-house then hire experienced managers to operate them, they have a concentrated portfolio of 10-12 companies / fund, and they are very low key: no blogging, tweeting, etc.

The fund was founded by Peter Svennilson and Dave Goeddel. Dave was the one of the first scientists at Genentech and perhaps the most important person at the company along with the cofounders, Bob Swanson and Herb Boyer. He is a legendary scientist who helped create the biotech industry by cloning the first human proteins in the late 1970s (at the same time that Apple was working on the Apple 2 and Microsoft was moving its headquarters from Albuquerque to Seattle). TCG’s other partners and investment professionals are all accomplished scientists, and their advisory board consists of Nobel Laureates and other highly esteemed scientists.

TCG invests in areas that other biotech VCs shy away from, including cardiovascular disease, metabolic disease and neurology. Like most other biotech VCs, they are also very active in oncology. They typically focus on ambitious scientific platforms rather than asset-centric “build to buy” investments (a “build to buy” investment is one where investors identify a gap in a big pharma’s portfolio, create a company to develop a drug to fill that gap, and then flip the asset to a big pharma company), but many of their companies end up being acquired nonetheless (that said, Flexus certainly had elements of a build-to-buy company).

TCG Fund 2

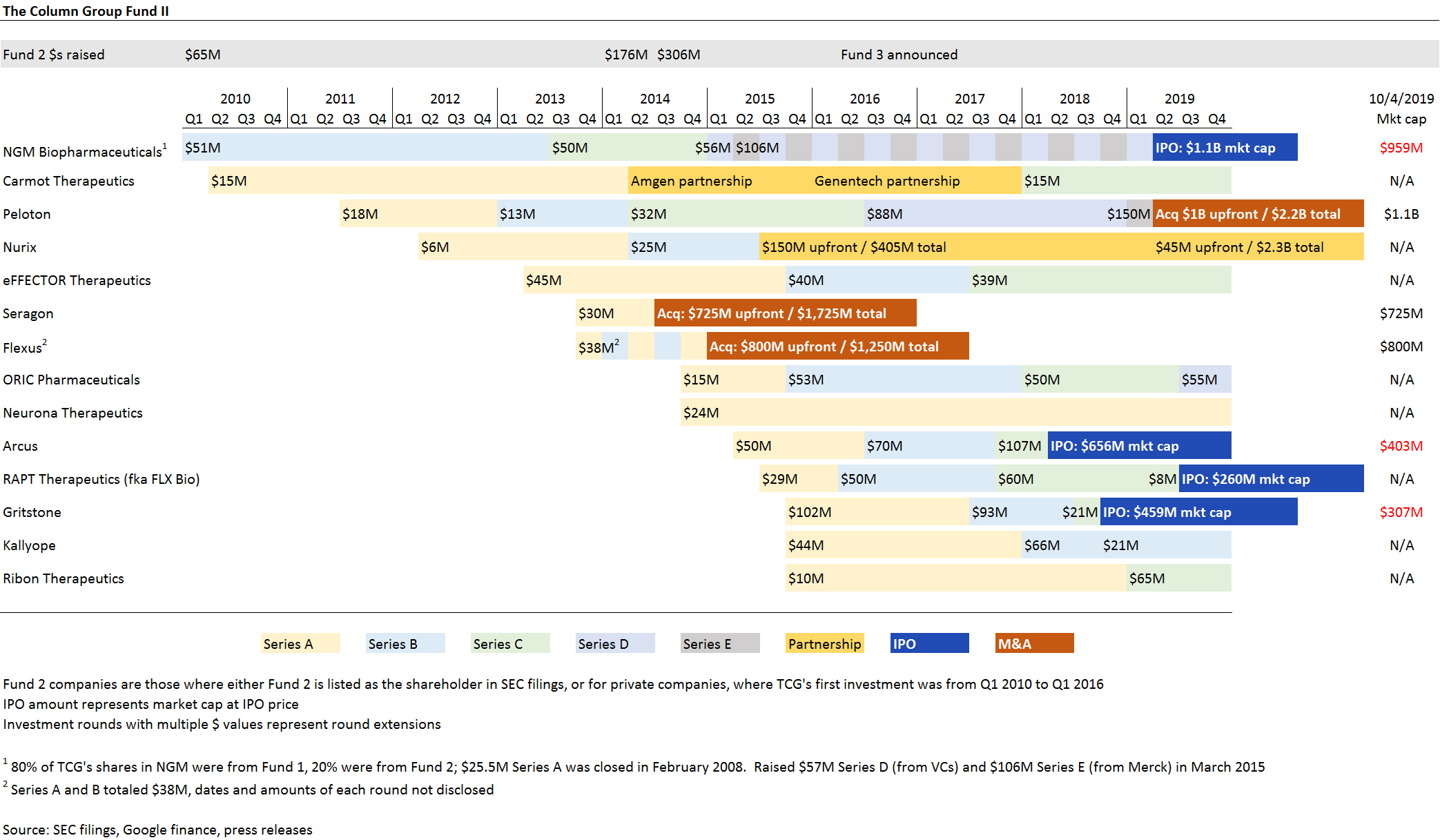

TCG’s second fund was a $322M fund that had its first close of $65M in 2010 and final close in 2014.

Apparently, it was tough for them to raise this fund. In 2010, the biotech startup world was at a low point. The entire financial industry was reeling from the financial crisis, there was no IPO window for biotech companies, pre-patent cliff big pharma wasn’t acquisitive, and most breakthrough science simply wasn’t working once it got out of the lab and into patients. TCG had always been focused on breakthrough early-stage science, but in 2010, early-stage biotech was almost as out-of-favor as residential mortgage-backed securities. A 2011 profile by Luke Timmerman (then at Xconomy, now the author of a great newsletter The Timmerman Report), highlights the challenges that TCG faced in raising this fund.

TCG Fund 2 invested in 14 companies by my count (this is in line with their stated strategy of investing in 10-12 companies per fund). Six of those have exited (one exit, NGM Bio, was funded through both TCG Fund 1 and TCG Fund 2). Three M&A exits generated the majority of TCG’s proceeds. Overall, TCG roughly doubled its fund based on these exits.

Of TCG’s other eight Fund 2 investments, all but one seem to still be alive. Two have done multiple big pharma partnerships, which may have generated some proceeds for TCG. Five others have recently raised large venture rounds.

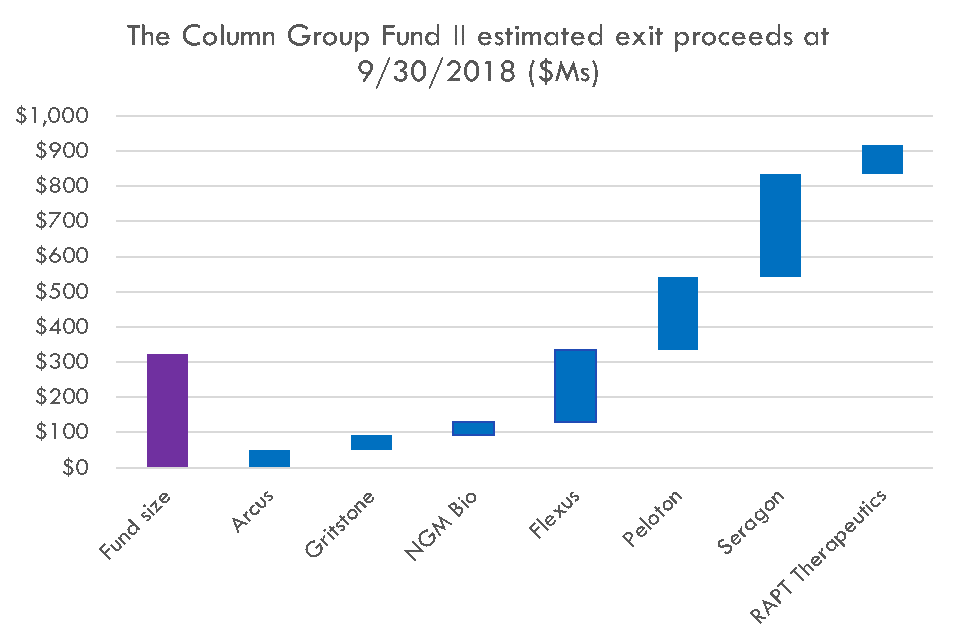

I estimated the proceeds generated by these exits as of September 30, 2018, which is the date of the IRR in the above Preqin chart, except for companies that went public or were acquired after that date – in which case I valued the companies at IPO price or price at M&A.

TCG had 3 investments that generated $200M+ in proceeds each. Another 3 exits generated $100M.

For Seragon, I estimated proceeds based on the TCG’s ownership at time of acquisition (which they conveniently publish here). Seragon was acquired for $725M upfront and up to $1,750 including milestones; I assume the total value is the average of the upfront and total potential value. Peloton was acquired for $1.1B upfront and $2.2B total including milestones; I exclude the milestones as the company was acquired recently so has had less time to achieve milestones. For Flexus, I assume TCG owned 20% at exit (this Fortune article says KPCB owned 30%, so I assume TCG owned a bit less).

While this was an impressive fund, it is unclear how Preqin got the 367% IRR for this TCG fund. My guess is that it came down to timing in the IRR calculations. Preqin lists the fund as a 2014 vintage, although the first close for the fund occurred in early 2010. Seragon and Flexus were large and very early exits –July 2014 and February 2015 respectively – and the timing of those exits shortly after the final close of the fund could have made the fund IRR very high, depending on the exact timing of cash flows.

In any event, TCG has more than doubled its fund just 5 years after the fund was closed and they have seven late-stage investments that could exit in the near term. Two of these un-exited companies have done large partnerships: Nurix has two partnerships worth almost $200M upfront and over $2.7B total, and Carmot has done two partnerships (one with Amgen, one with Genentech) but has not disclosed financials for these.

Foresite

Foresite was founded by Jim Tanenbaum, a successful biotech serial entrepreneur. Jim founded GelTex Pharmaceuticals, which was acquired for $1.6B in 1999, and Theravance, which split into two companies that have combined market cap of $3.3B. Foresite’s other partners come from diverse backgrounds including traditional biotech VC as well as computational biology backgrounds (including Verily’s former Chief Science Officer).

Foresite’s initial $100M fund was raised in 2012. This was a growth equity / public equity fund focused on healthcare. From what I can tell from their SEC filings, most of their investments were in public companies. Therefore I won’t spend as much time analyzing this fund, as it wasn’t a traditional venture fund.

Foresite I’s strategy was the perfect strategy at the perfect time: in 2011-2013, public biotech valuations were very cheap compared to current and historic levels. There were many high-quality late stage public assets available at good prices. The biotech market started heating up around 2013-2014: the IPO window reopened after a nearly decade-long drought, and big pharma companies began buying innovative startups at a record pace. This rewarded investors like Foresite who recognized the opportunity in biotech while other investors were hesitant to invest in the sector.

Generalist public equity investors quickly took notice of these rising biotech returns and flocked to biotech stocks. Sophisticated investors like Foresite moved from investing in public growth rounds to “crossover” investing (funding the last private round) and, later, to traditional VC.

Today, Foresite is very much a true venture fund and has an interesting strategy that combines traditional biotech investing strategies with an internal bioinformatics platform and an incubator for companies using technology at the intersection of biology and big data. It has had some great exits from its venture portfolio, most notably 10X Genomics. 10X went public in September 2019 at a ~$4B valuation, and Foresite is the largest institutional shareholder.

Defensible clinical trial cost estimates

Get transparent cost estimates for any trial in minutes. Input an NCT ID or upload a protocol, then see a full cost analysis report.

Flagship Pioneering

Flagship, like TCG, is a leading early-stage biotech fund focused on in-house company creation. Flagship has a unique company creation process in which young scientists collaborate with senior partners to create and test “venture hypotheses”. The most promising ideas are tested in the wet lab, and if the science works, additional capital is deployed against the opportunities. Flagship typically funds these companies through Series A and then syndicates later rounds. For a great overview of Flagship’s strategy, see this talk from Flagship Managing Partner Doug Cole at Columbia.

Flagship’s investments tend to be in companies developing novel platforms: mRNA therapy (Moderna), red blood cell therapy (Rubius), CRISPR gene editing (Editas), microbiome therapy (Seres, Evelo), glycans (Kaleido), combinations of metabolic compounds (Axcella), and others. They also fund non-therapeutics companies (Indigo Ag, TransMedics).

This contrasts a bit with TCG’s strategy, which focuses more on traditional modalities (small molecules, biologics) but builds companies around new insights in biology or biochemistry (although TCG certainly has gene and cell therapy companies, especially in its latest funds). Both funds have some element of contrarianism (Flagship’s focus on non-traditional modalities and “out there” science, TCG’s willingness to have a concentrated portfolio and take on risks that others might shy away from). TCG also has more M&A exits than Flagship: by my count, no Flagship Fund IV companies exited via M&A.

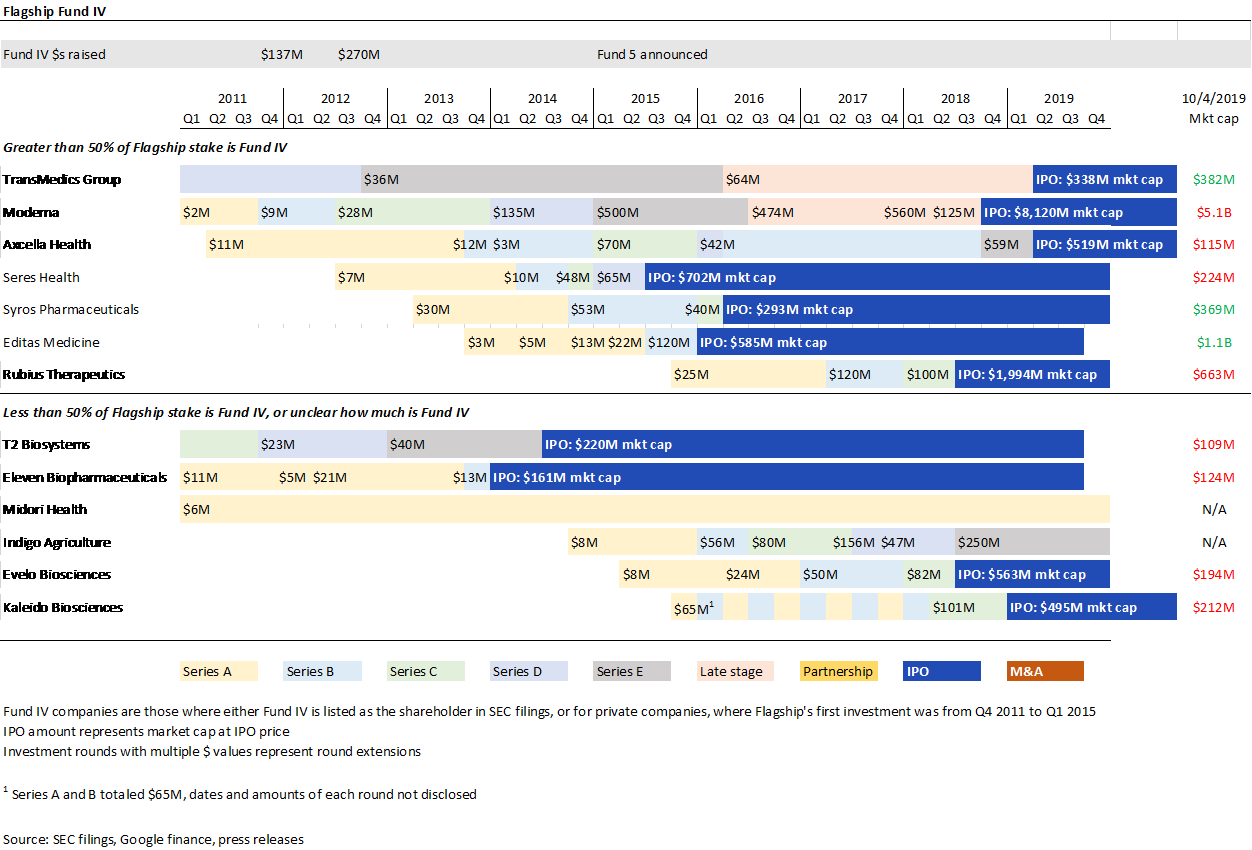

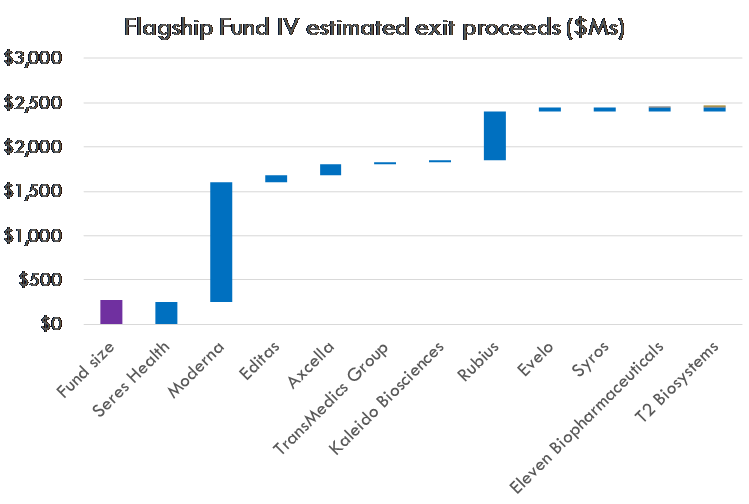

Flagship Fund IV

Flagship Fund IV, the fund highlighted in the above chart, was a phenomenal fund, but Flagship’s other funds also generated impressive returns from investments in companies like Receptos (acquired for $7.2B in 2015), Agios (public company with $2B+ market cap and 2 approved drugs), Denali Therapeutics ($1.5B market cap) and many others.

I was able to find 13 investments from Flagship Fund IV. Eleven of these companies went public. The combined market cap of these companies at the time of IPO was $14B, and the average market cap was $1.3B. Flagship owned on average 28% of these companies at IPO.

That is pretty amazing.

None of them have been acquired to date. Only one (Midori Health) seems to be dormant, and I’m not even sure that this was a Fund IV investment (the company was founded in 2011, during the investment period for Fund IV), but I found no more details. One other company, Indigo Ag, recently raised a very large round and seems likely to be a winner, although I’m not sure if this is a Fund IV investment (like Midori, it was founded during the Fund IV investment period, but I haven’t seen data confirming it is a Fund IV deal).

This is almost certainly not a complete list. When this fund was operating, roughly 75% of Flagship’s portfolio companies were built in-house. Per its website, Flagship started 6-8 “protocos” per year. Many of these died before raising Series A investments – Flagship does not even name these companies to reduce emotional attachment to the ideas and ensure that go / no-go decisions are made with objectivity. Flagship often does not issue press releases even when these companies raise Series A rounds (which are in some cases fully funded by Flagship), so it is hard to know how many companies Flagship funded.

Further complicating things, Flagship invests in many companies from multiple funds. For six of the thirteen Fund IV investments I found, less than half of Flagship’s investment came from Fund IV (the rest came from other Flagship funds).

Even if Flagship had 20 other Series A investments that failed from this fund, having 33% of the portfolio IPO at average market cap of $1.3B and average ownership at IPO of 28% is amazing. This portfolio combines the best of “power law” investing with the best of capital-efficient, low loss-rate biotech investing.

Flagship’s Fund IV appears to have a lower IRR than TCG’s fund, but a higher cash-on-cash multiple. By my count, as of 12/31/2017 (the date Preqin calculated the IRR) Flagship’s $270M fund was worth $2.5B – 9x the fund size (for portfolio companies that IPO’d after 12/31/2017, I valued them at their IPO price).

The Moderna investment is one that even the biggest unicorn-chasing VCs would envy. At the IPO valuation, Flagship’s stake was worth $1.5B (the stock has lost 12% of value since IPO – not very good, but not as bad as Uber, Lyft or WeWork).

Moderna alone would return 4x Flagship’s Fund IV at IPO valuation. But excluding Moderna, the fund would still be a 4x! That’s what happens when you start companies in-house (low valuations, aligned incentives for disciplined go / no-go decisions), can fund companies until they’re valuable enough to syndicate deals at attractive valuations, and have 11 portfolio companies that IPO.

Rubius was another huge win for this fund, but investments in the other smaller exits definitely add up (though it may not look like it in the chart, because the y-axis increments are $500M).

However, the investments have not performed as well in the public markets. Assuming Flagship held its stakes through 9/30/2019, Fund IV is worth $1.4B ($500M excluding Moderna). Still a very strong 5.3x return on the fund.

Orbimed

Orbimed is a massive healthcare investment organization. In addition to managing some of the largest healthcare venture funds, Orbimed also manages large healthcare focused hedge funds. In total, Orbimed manages $13B in healthcare investments globally.

Orbimed is a later-stage investor than Flagship or TCG. Orbimed does start companies in house, but takes a more hands-off approach (in contrast to TCG and Flagship, where investment professionals take active operating roles in the early stages of their portfolio companies’ lives). Orbimed also has a larger international presence than Flagship or TCG.

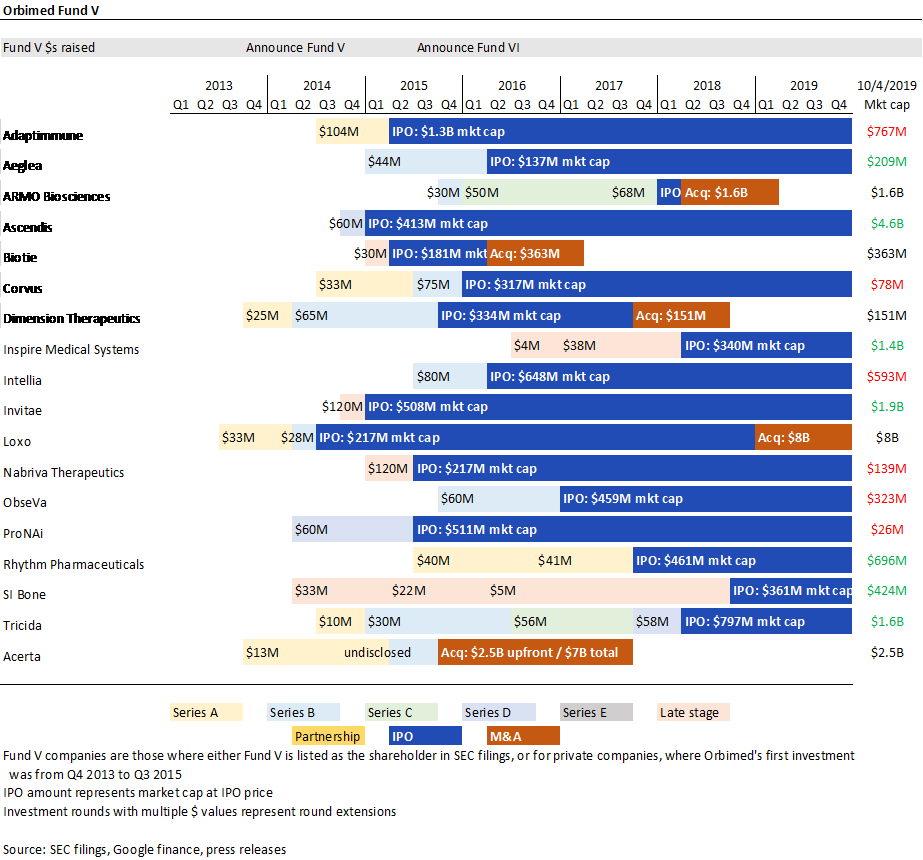

Orbimed Fund V

The $735M fund listed above is Orbimed’s 5th private equity fund. The fund was raised in 2013 and invested from 2013-2015. This fund was later stage than TCG or Flagship but earlier-stage than Foresite’s. From what I can tell, a bit under half of their initial investments were Series A, but most were Series B and beyond. Many were crossover deals, where Orbimed would fund the last private round and the company would go public soon after their investment.

The years 2013-2015 were a great time for this strategy, as the public markets were opening after a decade-long drought, and there was a huge backlog of high quality late-stage private companies. As one of (if not the largest) healthcare funds in the world, Orbimed undoubtedly had great access to deals and presumably helped companies access the public markets. Of the 18 investments I attributed to Orbimed Fund V based on public information (as I’ll discuss below, this is not a comprehensive data set), 17 of them went public (the 18th, Acerta, was acquired for $2.5B upfront / $7B total while still a private company).

Every company in the above list exited, with 17 IPOs. Though I attempted to find all of Orbimed’s Fund 5 investments, I can’t guarantee that this is a comprehensive list. I looked at SEC filings with Orbimed Fund 5 as well as all the press releases on Orbimed’s website from the period between 2013 and 2015, but I can’t guarantee that this list represents every deal Orbimed did.

Regardless, it seems like Orbimed had a large percentage of successfully exited investments. The IPO market was at its peak during the 2013-2015 period where they were investing this fund, and Orbimed was probably the largest late-stage biotech VC at that time (and still probably is today) and also had an active hedge fund, so it makes sense that they had a good batting average with IPOs.

Orbimed also had several nice M&A exits from this fund. ARMO was acquired for $1.6B shortly after its IPO, Loxo was acquired for $8B five years after its IPO (public market investors did phenomenally well with this investment – Loxo’s market cap at IPO was just $217M), and Acerta was a huge win for Orbimed. Because Acerta was acquired as a private company, we don’t know for certain how much Orbimed owned, and there were also milestones involved that we don’t know if they hit, but this may have been the best investment from this fund.

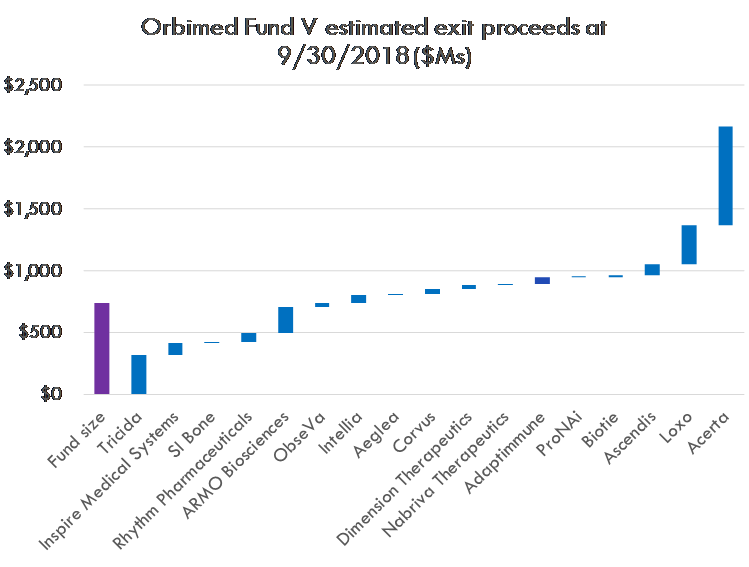

By my count, Orbimed returned a ~3x on its $735M 5th fund through 9/30/2018 as well as 9/30/2019.

As mentioned above, a major caveat is that Orbimed’s stake in Acerta, which was acquired for $2.5B upfront and up to $7B total, was not disclosed, as Acerta was private at the time of acquisition. I estimate Orbimed owned 20% at exit, and that Acerta received $4B in proceeds ($2.5B upfront + $1.5B unconditional milestone payments). Because Acerta is the fund’s best returning investment from what I can tell, this is an important assumption.

That said, not every company did well post-IPO. Overall, the post-IPO gains roughly cancelled out the losses: Fund V’s value is roughly the same whether you value portfolio companies based on their IPO price, 9/30/2018 stock price, or 9/30/2019 stock price. And even though there were 18 exits, the returns are highly concentrated in a few investments: Acerta, Tricida, Loxo and Armo. Without Acerta, Orbimed would have doubled their fund in five years – still quite impressive for a $735M fund – but it may not have cracked the top 10.

Defensible clinical trial cost estimates

Get transparent cost estimates for any trial in minutes. Input an NCT ID or upload a protocol, then see a full cost analysis report.

Portfolio strategy is about more than just decacorns

In another post, I analyze the returns of some of the best-performing tech and biotech startups of recent years. Both sectors generated amazing returns, but the best tech investments generated significantly higher cash-on-cash returns than the best biotech investments.

But biotech funds outperform tech funds. And not just on average – based on this Preqin analysis, the best biotech funds outperform the best tech funds. Of course we must consider the major caveat that not all funds disclose their returns, but based on the data I have access to, the best biotech funds beat the best tech funds.

Over the last decade, biotech has benefited from a perfect storm of innovation and a changing industry that favors startups. In addition to these tailwinds, biotech investors benefited from being in an “unpopular” sector, so were able to take their pick of the best investments and invest at favorable valuations.

However, generalists have flocked to biotech in recent years. The public market and late-stage private markets are very crowded. Series B investing had been quite crowded until Chinese investors withdrew in late 2018 / early 2019 due to trade tensions, and Series A investing is still dominated by the same funds that were leading 10 years ago.

But the seed investing market is wide open. Early-stage Series A VCs are active seed investors, but they focus on companies they fund in house, rather than on founder-driven companies. The First Round, Lowercase Capital and Y Combinator of biotech have yet to be created. As I discuss in another post, the biotech versions of these funds won’t look like the software-focused originals.

You may also like...

Top biotech VCs of 2018 and 2019

Valuing drugs and biotech companies

Venture returns from biopharma IPOs, 2018-Q1 2019

Valuations of biotech startups from Series A to IPO

Did you enjoy this article?

Then consider joining our mailing list. I periodically publish data-driven articles on the biotech startup and VC world.