Biotech from bust to boom

February 28, 2022

The last ten years have seen biotech enjoy the biggest and most durable boom in the industry's history. But the future is uncertain: the public market and IPOs are down, but venture funding is still near all-time highs, and there have never been as many innovative companies and technologies.

To help understand where the market may go from here, this post will describe the biotech boom of the last decade: the phases of the boom, what factors drove the boom, and how the market has changed.

Subsequent posts will place the current market in historical context, specifically with respect to 1) investor risk tolerance and 2) level of fundamental innovation. These posts will discuss where the industry and market may go from here, and how companies and investors can plan for various scenarios.

To receive an email when we post new articles, sign up for our newsletter here.

Bust to boom

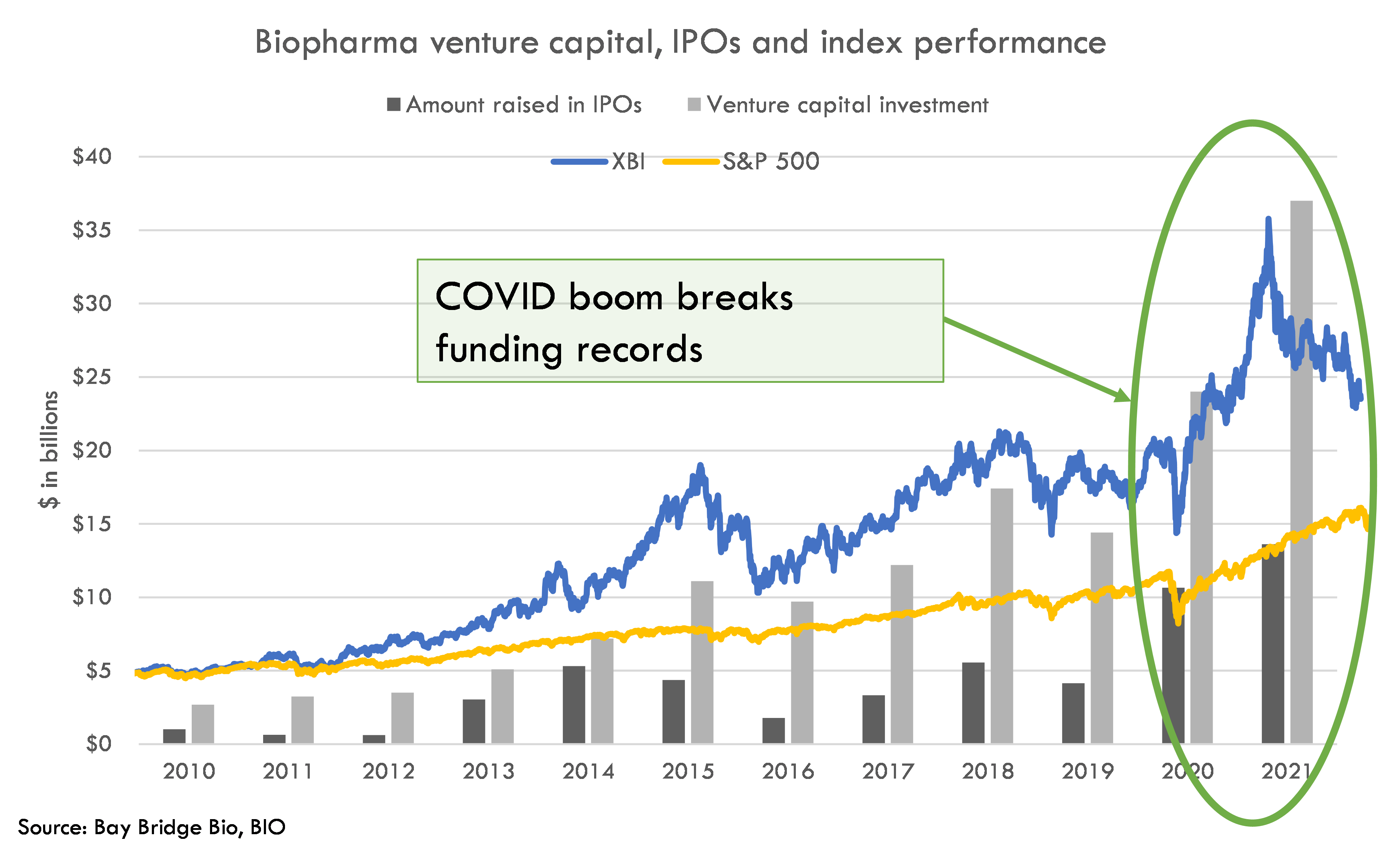

Despite biotech’s poor performance over the last year, the industry is still in the midst of a historic boom. This boom followed a decade-long slump, starting with the dotcom / genomics bubble bursting, and ending a few years after the 2008 financial crisis. From 2003 to 2011, around $4B was invested annually into biotech startups. That’s more than 9x lower than the $37B invested in 2021.

The bust-to-boom story is also exemplified by the IPO market. From 2007 to 2009, there were no biopharma IPOs for nearly two years, until Cumberland Pharmaceuticals went public. Two years without biopharma IPOs is almost unimaginable today.

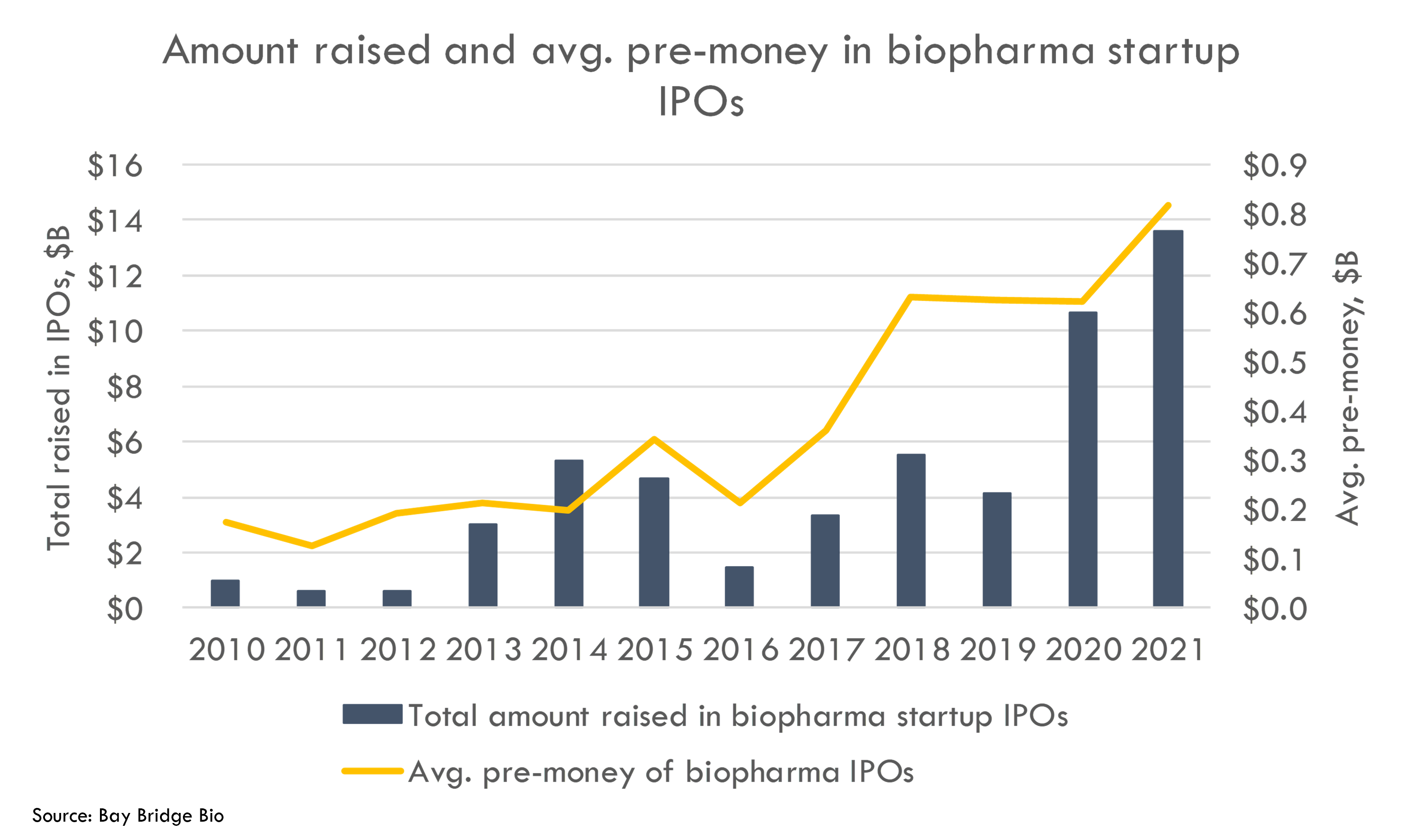

Fortunately, that drought was short-lived. Starting in 2013, the biopharma IPO market took off.

The IPO market picked up from 2010 to 2017, with an average IPO pre-money of $246M and a total of 24 preclinical IPOs (representing 9% of biopharma IPOs). This boom accelerated over the last 4 years: since 2018, the average IPO pre-money was $691M, and there have been 52 preclinical IPOs (representing 23% of biopharma IPOs). The IPO market's rise has paralleled a general increase in investor risk tolerance.

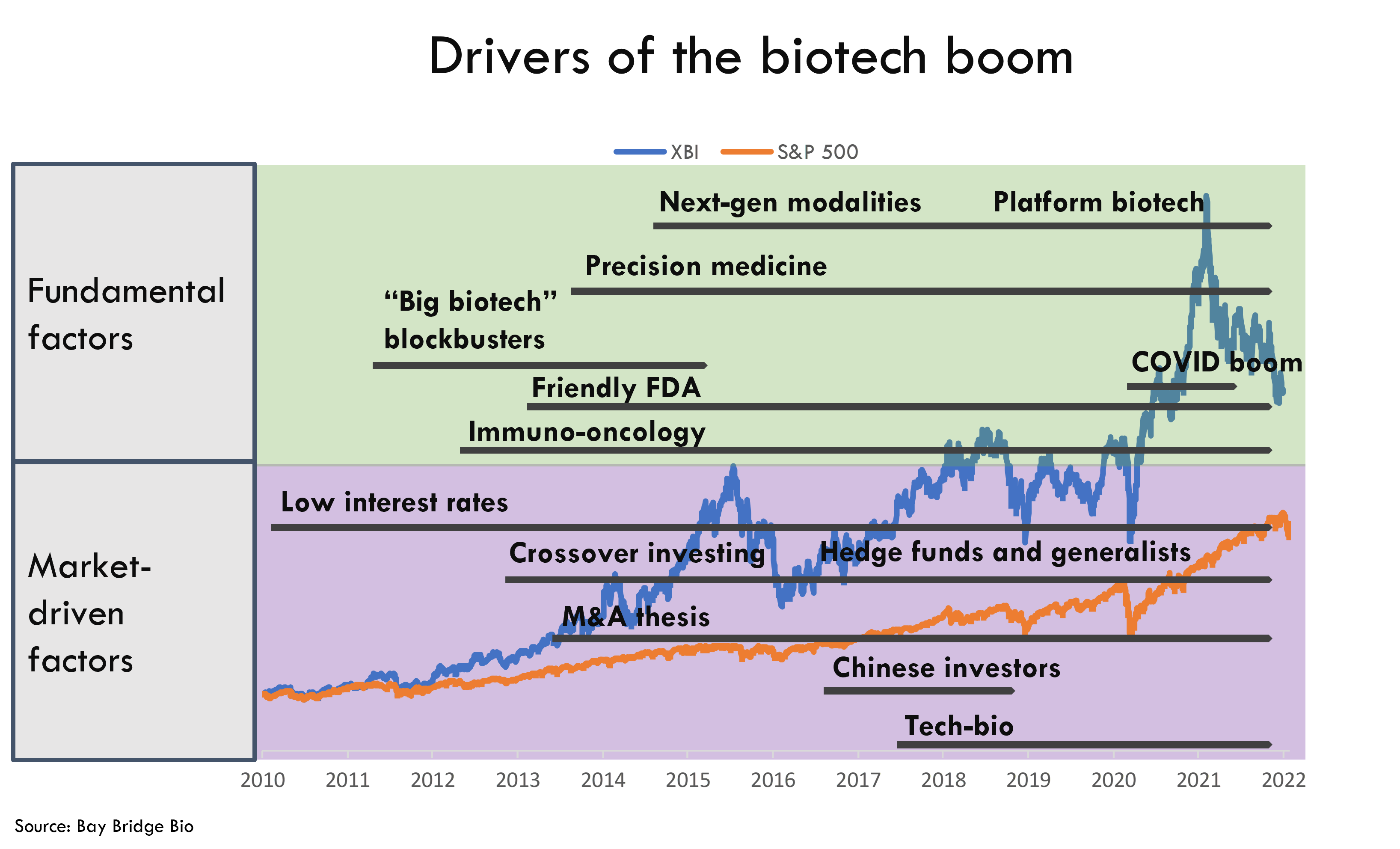

Drivers of the boom

What drove this boom in venture funding and IPO activity? We break down the drivers of the boom into two components: “fundamental” and “market-driven”.

- Fundamental factors are things that make biopharma companies inherently more valuable, in terms of the expected value of future cash flows generated by companies. These include profitable new products; strong clinical data for new classes of drugs; a more supportive regulatory environment; and scientific breakthroughs that enable more valuable drugs to be developed, or that allow drugs to be developed more quickly or cheaply.

- Market-driven factors represent changes in the market’s perception of value. This is often due to new investors entering or leaving the market, or changes in investor sentiment. These factors include pharma being more aggressive with M&A to replace off-patent drugs (one could argue that this is a fundamental factor as well, as it depends on the structure of the pharma industry), more generalist investors entering the market, or changes in sentiment.

These factors are related. Usually changes in fundamentals drive changes in market-driven factors, but the market does not always correctly value changes in fundamental factors. If market-driven factors misprice the impact of changes in fundamental factors, the market becomes over- or undervalued (the Gartner hype cycle illustrates this dynamic).

Especially in hot markets, it can be difficult to tell the extent to which a company is valuable because of fundamental factors or market-driven factors. But differentiating between these two sources of value is critical. Investors who focus on fundamentals in a speculative market can be stuck on the sidelines. But investors who ignore (or misvalue) fundamentals are left holding the bag when sentiment sours.

We can't predict the market, but studying the recent history of the market can shed light on how much risk the market currently bears.

In the wake of the financial crisis, biotech was battered and bruised after a decade of poor performance. The next-gen science that arose in the genomics bubble of the late 1990s wasn’t working, FDA had taken a very conservative stance on approving new drugs, and big pharma’s “patent cliff” was eroding billions of dollars of revenue. What changed?

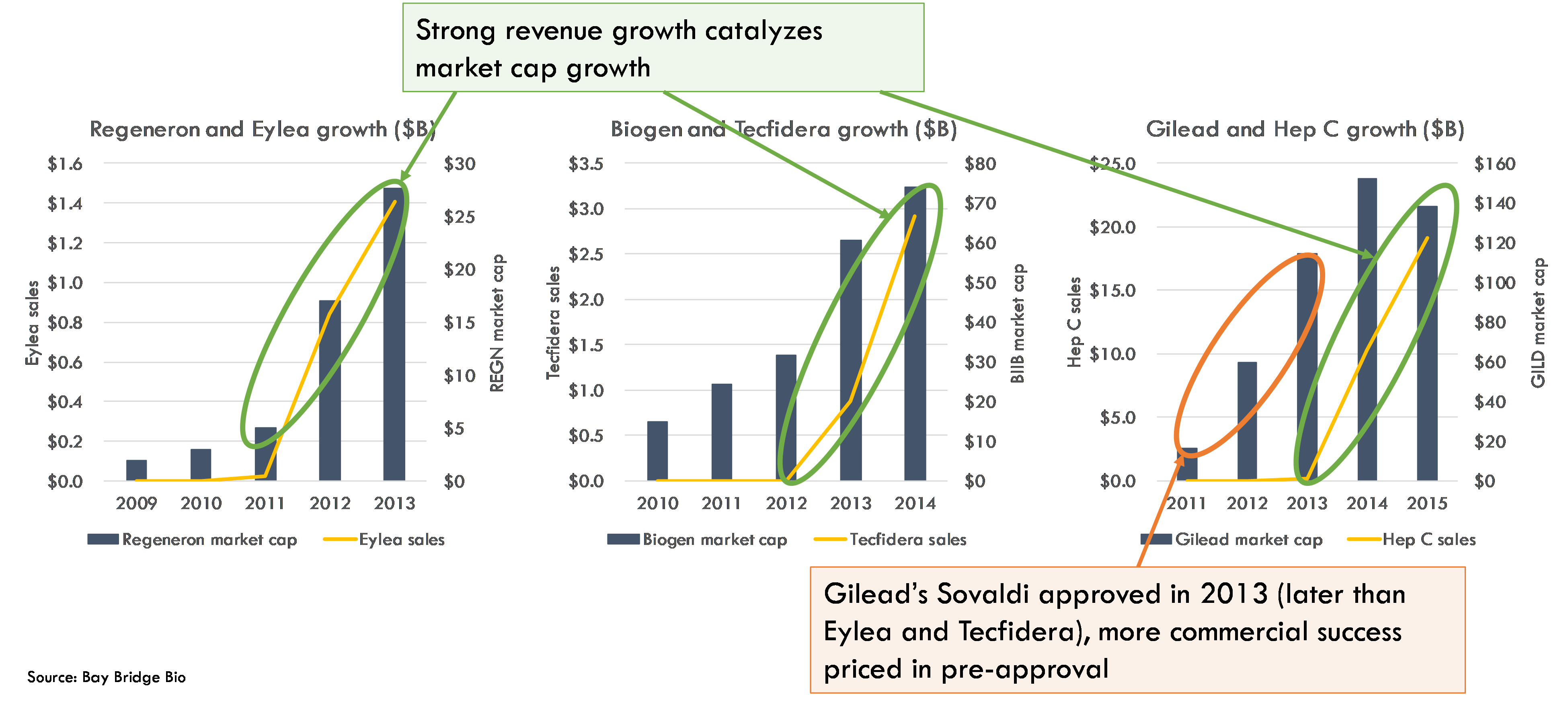

"Big biotech" blockbusters

The first "fundamental factor" that drove investor interest was the successful launch of several “big biotech” drugs in 2012-2014, including Regeneron’s Eylea for wet AMD, Biogen’s Tecfidera for multiple sclerosis, and Gilead’s Harvoni and Sovaldi for hepatitis C.

These drugs had incredibly successful launches, going from zero to several billion in just two years (Gilead’s Hep C drugs went from $0B to $10B in just one year on the market, a record prior to the COVID vaccines from MRNA and Pfizer/BNTX). These successful launches reignited investors’ interest in biotech, demonstrating how rapidly drugs can grow if they provide significant clinical benefits to patients.

One notable feature about these drug launches is when the stocks priced in commercial success. These stocks took off once their drugs generated strong sales. Before these companies proved their drugs’ worth with actual revenue, investors did not give the products much credit (“short the launch” was a common theme around this time). When these drugs had better-than-expected launches, investors rewarded them.

These successes renewed interest in biopharma and gave investors more confidence in investing in clinical-stage companies. Of the three drug launches highlighted above, Gilead’s Sovaldi launched last. Investors began to bid up the valuations of late clinical-stage companies in 2013, so by the time Sovaldi was approved in December 2013, Gilead’s market cap had already nearly doubled from $60-120B in 2013. Because Biogen and Regeneron’s drugs were launched before biotech was “rediscovered”, their largest gains in market cap came after Tecfidera and Eylea were launched in and generated tremendous growth.

Another way of saying this is that from 2009-2012, commercial success was not priced in, even if drugs were approved and clinical risk was eliminated. Prior to 2012, biotech was in “risk off” mode, and did not even take on much commercial risk. After the success of these launches, however, the market began to price in commercial success based on clinical data.

Defensible clinical trial cost estimates

Get transparent cost estimates for any trial in minutes. Input an NCT ID or upload a protocol, then see a full cost analysis report.

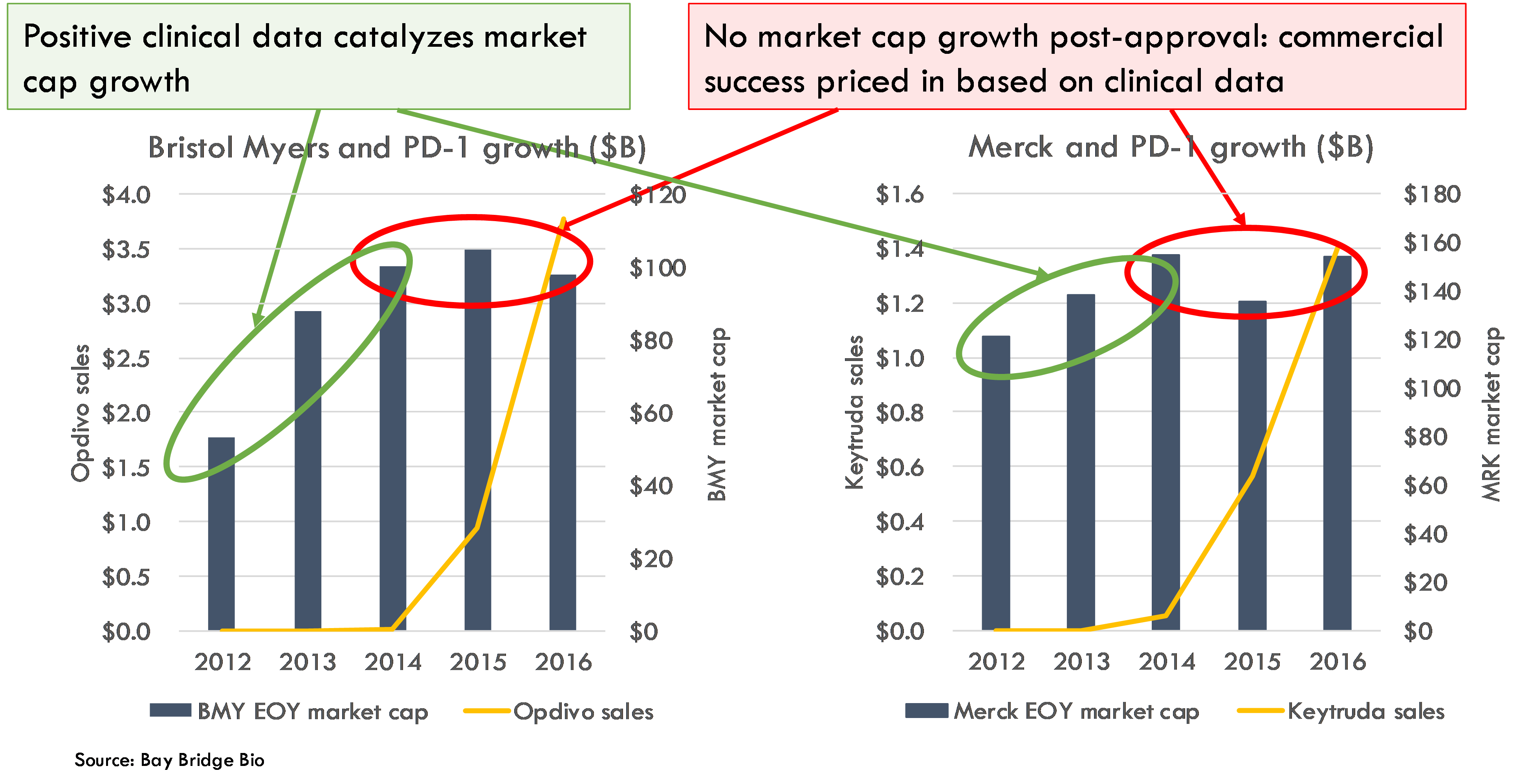

Immuno-oncology

The next big wave in biopharma was the immuno-oncology wave. Starting in 2013, PD-1 inhibitors (a type of immune “checkpoint” inhibitor) from Merck and Bristol Myers released incredible clinical data in treating cancer (CTLA-4 inhibitors, a class of checkpoint inhibitors that was developed before the PD-1s, also had solid data though not as strong). This set off a flurry of investor interest in other immuno-oncology companies, and a search for combination therapies that could be used to enhance the effectiveness of PD-1 inhibitors.

These strong clinical data translated to massive commercial success once these drugs were approved. Bristol Myers’ Opdivo generated $3.7B in revenue in its second year on the market, and Merck’s Keytruda generated $1.4B in its second year of commercialization.

However, this commercial success didn’t increase the stock price. In fact, both Bristol Myers’ and Merck’s market caps were lower two years after their PD-1 inhibitors were approved than they were in 2014, the year they were approved.

By the time these drugs were approved, the market had already priced in success. Bristol Myers’ market cap grew 65% (adding $34B in market cap) during 2013 as initial clinical data for BMY and Merck’s PD-1 inhibitors was released. Merck, whose pembrolizumab was considered second-best to BMY’s nivolumab at the time (though the tables turned in 2016-2018), gained $14B in market cap (a 14% increase from the prior year) in 2013. Both companies saw additional market cap gains in 2014 as more data were released.

But because investors priced in very strong commercial performance after they saw the clinical data, even the blockbuster launches these drugs achieved did not impress investors. Investors had continued to increase their risk tolerance.

Friendly FDA

An increasingly innovation-friendly stance at FDA added fuel to the fire of investor enthusiasm for immuno-oncology. Merck’s Keytruda (pembrolizumab) was one of the first drugs to receive Breakthrough Designation from FDA in 2013. Subsequently, both nivolumab and pembrolizumab received other Breakthrough Designations, Fast Track designations, and Accelerated Approvals for several indications. Many other developmental oncology drugs (and drugs for other diseases) also received these regulatory benefits, which reduced the time and cost, and increased the probability, of FDA approval. Many of the drugs that received these FDA designations were cancer drugs or drugs to treat severe rare diseases.

A friendlier FDA decreases the risk profile of investing in biotech. This encourages investors to fund earlier-stage companies. Because cancer and rare disease companies were some of the main beneficiaries of these regulatory developments, cancer and rare disease companies received the bulk of funding and investor interest starting around 2013. It is important to note that these companies did not become more valuable solely because of a shift at FDA -- these companies became more valuable because they were developing drugs that provided real benefits to patients with severe disease, and the regulatory changes were at least in part driven by a recognition that patients needed to get these drugs faster.

Precision medicine

Another tailwind for drug development, specifically for cancer and rare disease drugs, was the rise of “precision medicine”. Broadly, precision medicine refers to developing drugs for specific, genetically defined patient populations (as opposed to the broad patient populations for whom drugs had traditionally been developed). While the numbers of patients eligible for these treatments are smaller than for broadly developed drugs, the perceived probability of clinical success is higher, and the cost and time required to get to clinical proof of concept is lower (as trials could be smaller). Because these drugs often treat severe, life-threatening disease and are designed to provide dramatic clinical benefits, they could command higher prices than traditional “primary care” drugs, so they were still valuable despite lower numbers of patients.

Precision medicine and a friendly FDA reduced the (actual and perceived) clinical and regulatory risks and encouraged investors to take on early clinical risk, notably for cancer and rare disease drugs that benefited most from these tailwinds.

One way to demonstrate the level of early and late clinical risk that the market was willing to take on is to look at the market cap of clinical-stage biopharma IPOs by year:

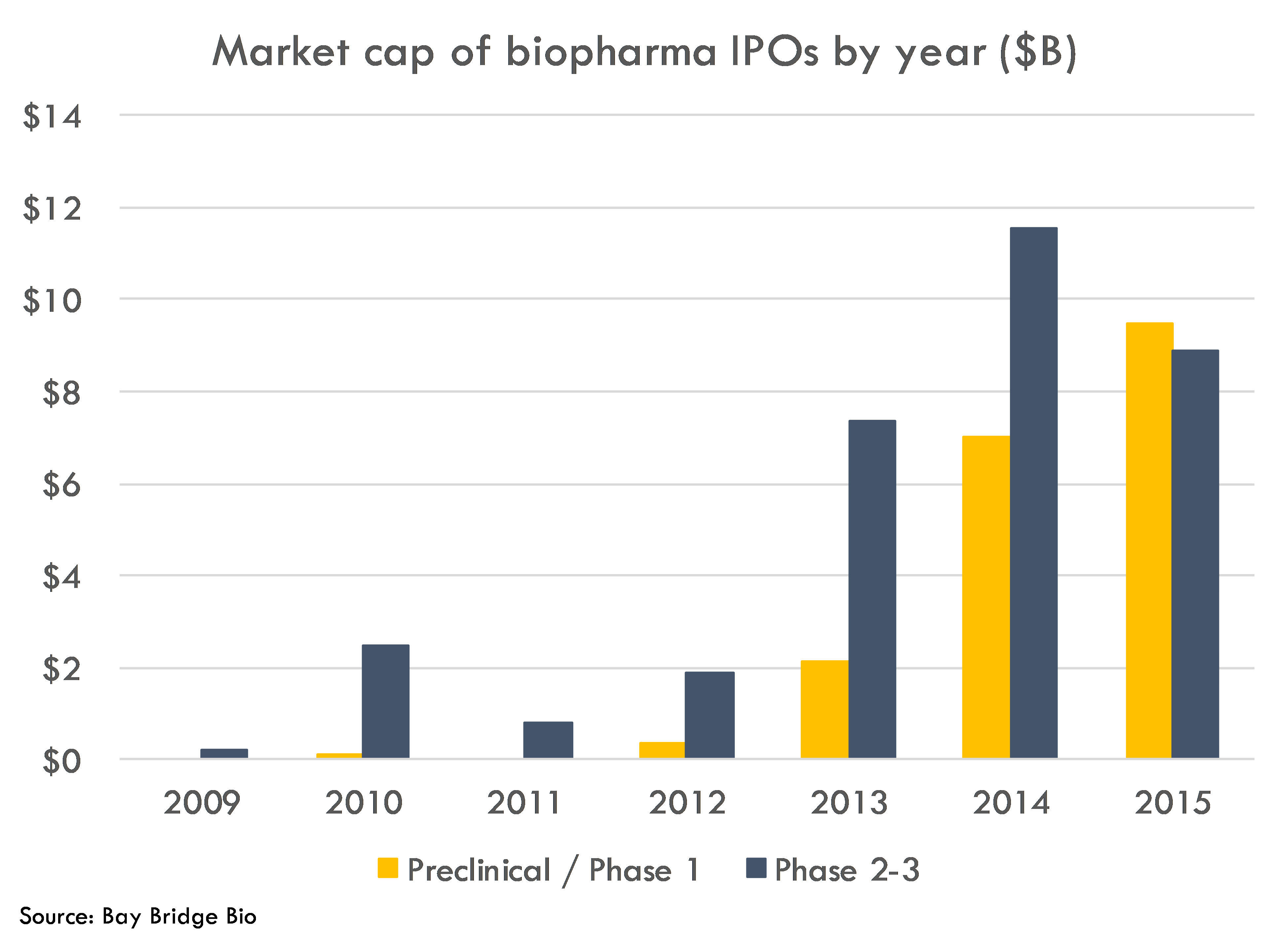

In 2013, there was a large jump in the value of Phase 2-3 IPOs as investors became more accepting of late clinical risk. By 2014, investors were generally open to clinical risk.

Investors continued to gradually become comfortable funding earlier-stage companies. In 2014, the IPO market opened up to preclinical and early clinical companies. Many of these companies were developing drugs for cancer and rare disease, driven in large part by the three forces mentioned above (immuno-oncology, a friendly FDA, and precision medicine).

Low rates and quantitative easing

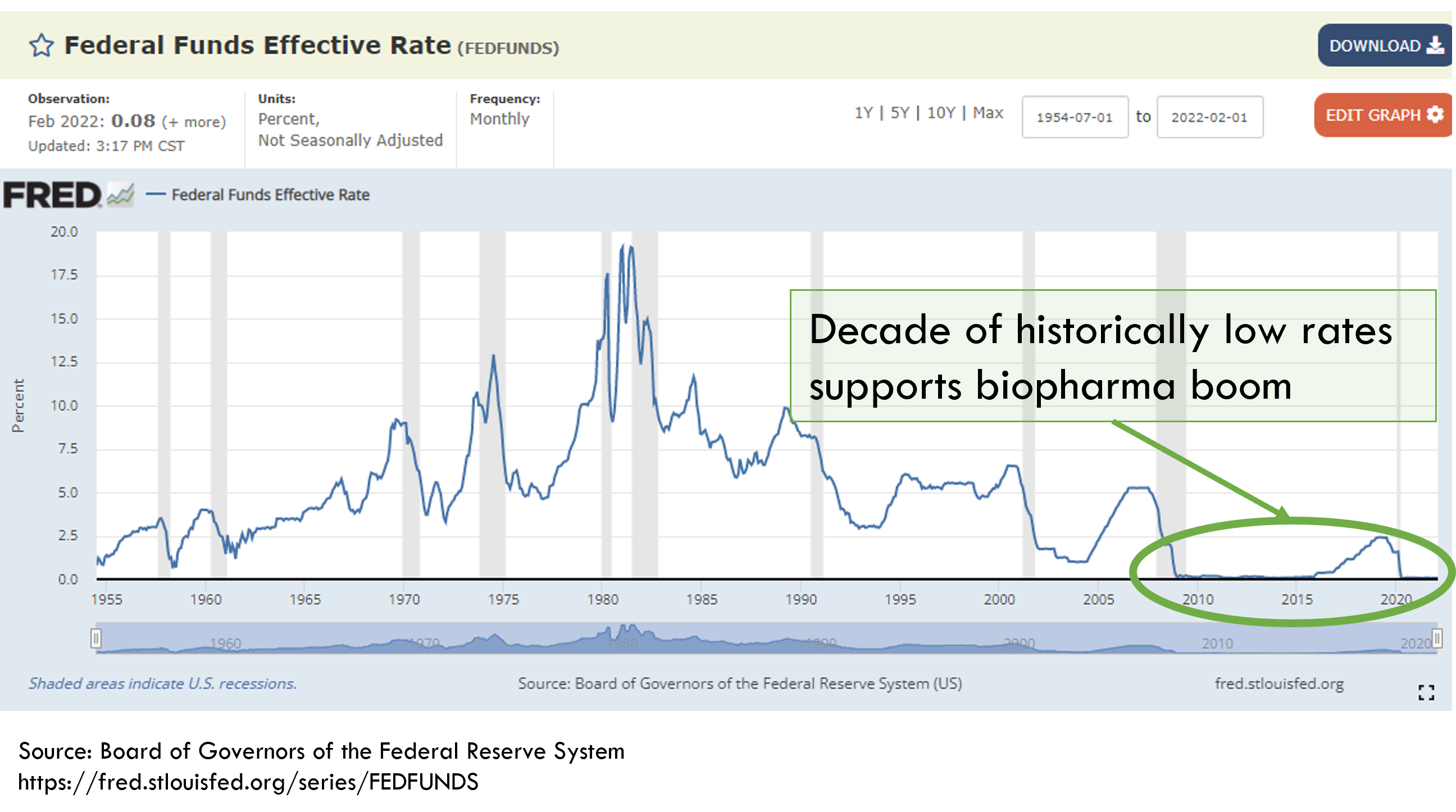

Underlying these fundamental factors was a powerful market-driven factor: accommodative monetary policy. The Federal Reserve, and most major central banks worldwide, cut interest rates to near zero during the financial crisis and embarked on major asset purchase programs and quantitative easing to support the financial system. With the exception of a few small instances of monetary tightening (all of which were reversed – and then some – at the start of COVID), the global economy has been supported by this accommodative monetary policy for over a decade.

While the impact of monetary policy on markets is a complex topic beyond the scope of this post, a discussion of the biotech boom requires some mention of monetary policy. Accommodative monetary policy generally increases investors’ risk tolerance and increases the prices of stocks and other assets.

When central banks reduce borrowing costs (essentially reducing the cost of money), this encourages borrowing and investment. As more money competes to invest in a given set of assets, the prices of those assets rise.

Low rates also decrease the returns generated by bonds. Investors who require a certain amount of yield (for example, pension funds that are underfunded and that must generate investment profits to fulfill their pension obligations) must turn to riskier investments than “safe” investments like bonds in order to generate returns. Lower interest rates also reduce the “required return” for investing in stocks and other assets – if bonds, a big alternative to investing in stocks, generate lower returns, then investors will accept lower returns from stocks, and thus be more willing to invest at higher prices. Low rates also decrease the discount rates investors use to calculate the present value of future profits, which further increases stock prices.

The ultimate result of these policies is that more money flows into the financial system. That money has to go somewhere. Initially, that money goes towards less-risky assets, increasing the price of those assets (and reducing the return). As more money enters the system and less-risky assets become increasingly expensive, investors look towards increasingly risky assets: venture capital, biotech, and crypto, to name a few.

Crossover investing and the IPO window

Several hedge funds and mutual funds noticed that these fundamental changes in the industry made a whole new class of companies eligible for the public markets. These companies were previously too risky for big public equity investors, but new scientific breakthroughs and FDA’s accommodative stance decreased the perceived risk of these companies (especially as these investors continued their search for yield as the low-interest Fed regime continued). Many of these big mutual funds also made a lot of money from investing in big biotech companies like Gilead, Regeneron, Biogen and Celgene, and were thus emboldened to wade more deeply into the biotech waters.

Funds like RA Capital, Fidelity, Perceptive, Orbimed, Foresite and Deerfield led the "crossover trade": using their knowledge of public markets and experience evaluating risky biotech investments to find private biotechs that would be good fits for big mutual funds and other public equity investors. These firms greased the wheels of the IPO market and helped public equity investors gain exposure to the most innovative companies.

This was overall a healthy development, providing new funding sources and liquidity for fundamentally sound yet undervalued companies and their investors. There was a tremendous backlog of strong private companies waiting to IPO after years of a closed IPO window, and the rise of the IPO market and crossover trade reflected a growing recognition of the fundamental strength of these companies. The years 2010-2013 were probably the best years ever to be a fundamentals-focused biotech investor.

The M&A thesis

These fundamental trends continued to mature through 2015, when the XBI hit a local peak and preclinical IPOs became more common (and more highly valued). Another major market-based driver eventually pushed the market even higher: the “M&A thesis”.

After the patent cliff in 2012 decimated big pharma revenues, big pharma had been much more acquisitive and was paying increasingly high sums for risky companies in an effort to replenish their pipelines. Around 2014-2015, many early-stage biotech companies began to trade more based on likelihood of an M&A takeout than based on fundamentals, shifting the market to a more speculative posture and away from fundamental-oriented valuation.

The upshot was that risk tolerance increased to a local peak, with investors more open to taking preclinical risk.

Rising rates and Martin Shkreli

In late 2014, the Federal Reserve announced that it was planning on raising rates for the first time since the financial crisis (the Fed communicates its plans meticulously and far in advance of executing the plans to avoid spooking the market). In December 2015, the Federal Reserve increased interest rates for the first time since the financial crisis and continued tightening through 2019.

The expectation of increased rates decreased investors’ overall risk appetite, which took the steam out of the market generally (the S&P 500 index dropped around 14% during this time), and the biotech boom specifically (pre-revenue biotech stocks are considered one of the riskiest asset classes, so if investors want to reduce risk, biotech is often one of the first sectors to get cut).

While the prospect of rising rates gradually deflated the market, Hillary Clinton’s infamous tweet in September 2015 about drug pricing reform put a pin in any biotech bubble that may have formed. The biotech market continued to deteriorate as drug pricing became a national concern during the runup to the 2016 presidential election, with the XBI bottoming in February 2016.

The prospect of rising rates combined with fears of drug pricing regulation led to the biggest drop in the biotech market since the start of the boom, with the XBI down 49% (the S&P 500 was down only 14% during this time).

As if this weren't enough, 2016 also saw a sharp drop in M&A and FDA approvals. The damage wasn't limited to the XBI: IPOs and venture funding was also down. Fortunately, these drops ended up being one-offs, with M&A, new drug approvals, IPOs and venture funding picking back up in 2017.

By 2017, the market had pulled back to a level we characterize as accepting “late clinical risk”.

Next-gen modalities

Sentiment in biotech had gradually recovered from 2016 lows, and in 2018 big pharma stepped up again to support the startup ecosystem, this time with big-money buyouts of companies developing next-generation platforms. Leaders in cell and gene therapy and precision medicine like AveXis, Kite, Juno, Loxo and Spark were acquired for multi-billion dollar sums, exciting investors with the prospect that big pharma would make big moves into next-generation platforms.

When these companies were acquired, their lead drugs were either approved or had very strong clinical data, so the stocks were already valued in the billions. But the big premiums paid by pharma for these platforms validated strategic interest in these platforms and led investors to speculate that an arms-race might develop among pharma companies hungry to become leaders of a new generation of pharma company built on cellular and genetic medicine.

The number of venture investments in and IPOs of cell and gene therapy companies increased significantly, and other next-gen modalities like gene editing, mRNA and other nucleotide therapies also garnered significant interest (culminating in MRNA’s December 2018 IPO at an $8.1B post-money).

While we call these modalities “next generation”, they weren’t new. Gene, cell and oligonucleotide therapy had been around since before the dotcom bubble, and genetic medicine was the top buzzword of the 2000s-era genomics bubble. After losing interest in these modalities in the 2000s, public market investors became reacquainted with them as early as 2014, when CAR-T companies Kite, Juno and Bellicum went public. These were big IPOs at the time, though the numbers are not surprising by the standards of the last few years: Kite raised $127M on a $500M pre-money while in a Phase 1/2 study, Juno raised $264M on a $1.6B pre-money during its Phase 1/2 study, and Bellicum raised $140M on a $350M pre-money.

Recession fears and reduced rates

There was limited market impact from new fundamental drivers from 2018-2019, and the XBI, venture funding and the IPO market were slightly down from 2018-2019. In late 2018, fears of a global recession led to market declines, but rate reductions in 2019 alleviated these concerns.

Despite occasional market corrections, like those in 2015 and 2019, the market overall was resilient and continued rising. The duration and magnitude of corrections was not sufficient to meaningfully and durably reduce risk appetite, so despite volatility, investors continued to increase risk appetite and search for yield.

One consequence of this stable increase in risk appetite is the rise of venture capital funding in biopharma. Because any slowdown in the IPO markets was not long enough or drastic enough to put a major dent in VC’s performance, VC returns remained attractive. Thus money continued to flow into private biopharma companies.

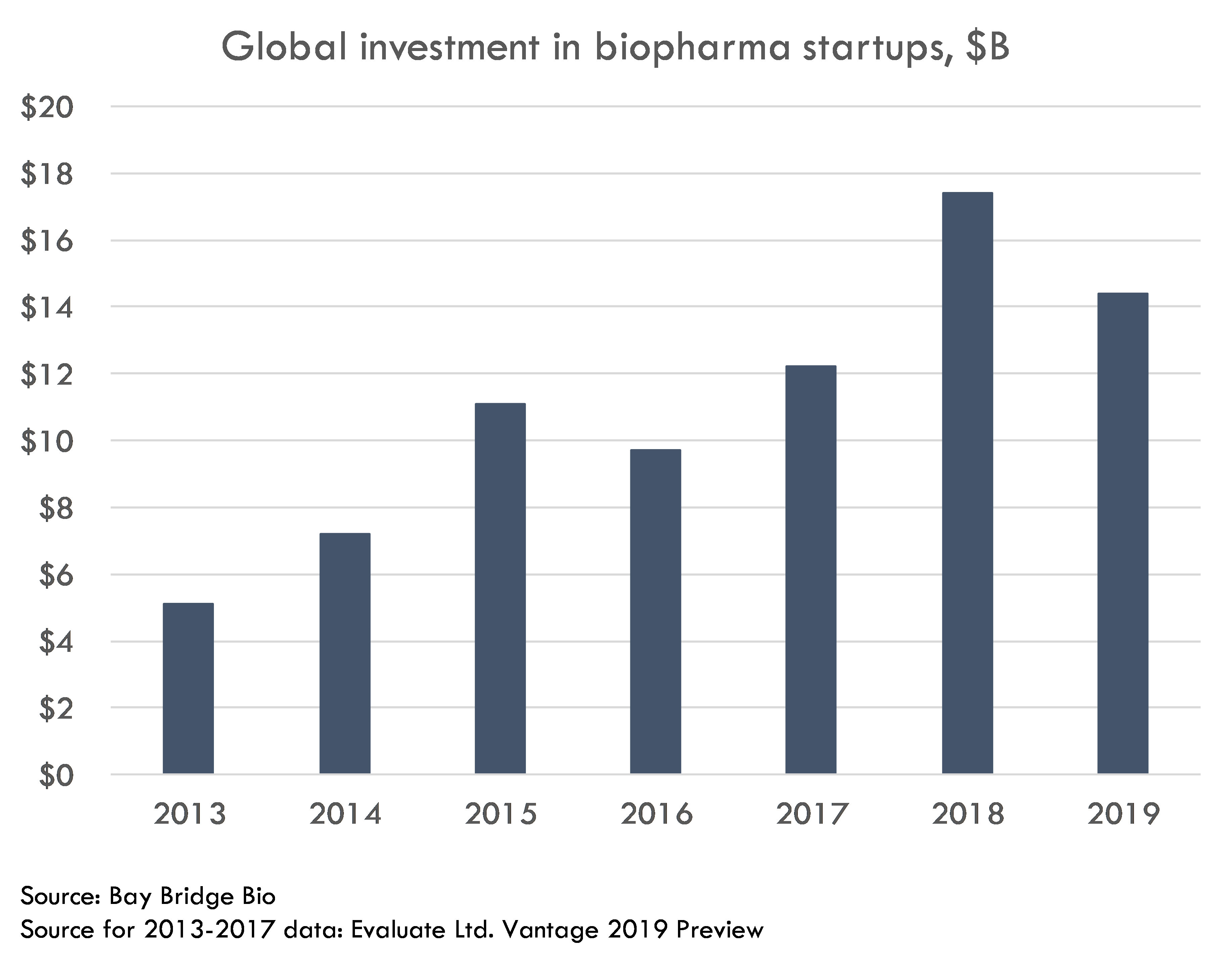

2018-2019 specifically saw the venture market supported by three major new entrants: Chinese investors and hedge funds piling into late-stage venture, and tech-bio investors (software VCs who began to invest in biotech, often “comp bio” platforms) entering early-stage venture (primarily at the seed-stage during the 2018-2019 timeframe, at least in biopharma).

While Chinese investors left the market as quickly as they entered due to global trade tensions, hedge fund investors and tech-bio investors gradually increased their activity through early 2020 and picked up activity significantly in 2021. By early 2020 (before COVID), the market was back to a level of risk tolerance similar to that of 2015.

The COVID boom

The biopharma market was already at a historically high level of risk tolerance by the beginning of 2020. COVID saw markets rise to new heights, and new levels of risk tolerance. After an initial crash due to COVID, the Fed quickly came to the rescue and sparked an unprecedented boom in biopharma investing.

The biopharma market benefited from two powerful tailwinds:

- A huge influx of new money into the financial system that increased the value of all risk assets, from SPACs to tech startups to crypto to biotech

- The astonishing success of mRNA-based COVID vaccines developed by Moderna and BioNTech

These tailwinds combined to spark an increase in speculation and risk tolerance in the biotech markets. A huge class of investors became aware of the potential for new modalities to deliver treatments that were previously considered out of reach, and the search began for the next big platform. 2020 and 2021 saw the rise of the ever-more ambitious “platform” company. These platforms ranged from companies that were similar to “traditional” biotech platforms, but with an extra dose of ambition and hype (Lyell, Sana, etc.), to newer platforms like comp bio (RXRX, ABCL, EXAI), and even to non-therapeutics biotech platforms (Zymergen, Gingko).

Investors in 2021 embraced platform risk, funding a class of some of the riskiest, but also most ambitious, companies in biotech. Investors were open to most scientific risk, although most investors were still not willing to take on as much "people" risk (the perceived caliber of management, investor syndicate and scientific founders and advisors is often core to the investment theses for these platform companies).

COVID boom vs. dotcom-era genomics boom

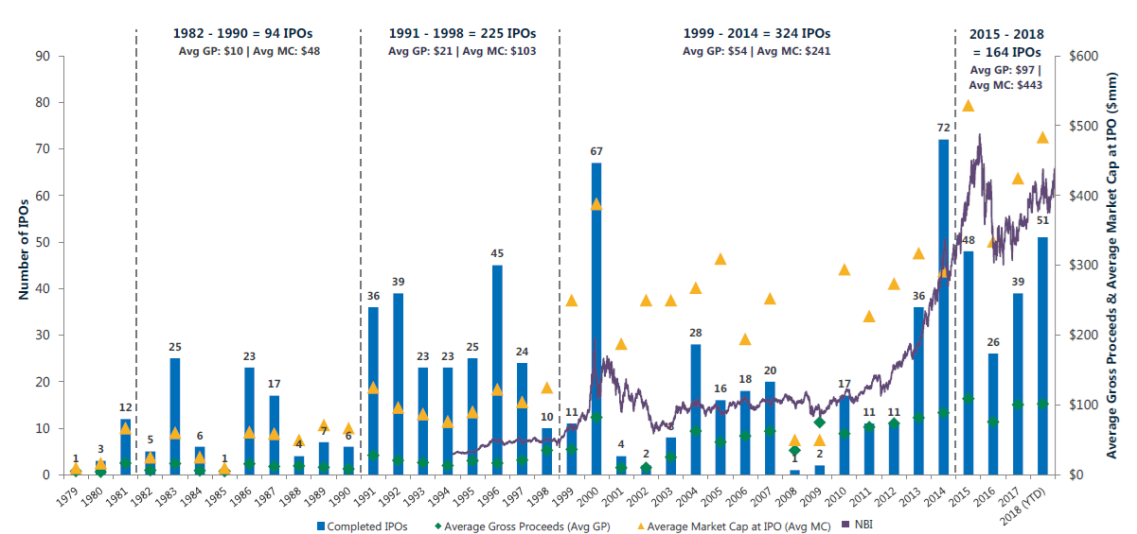

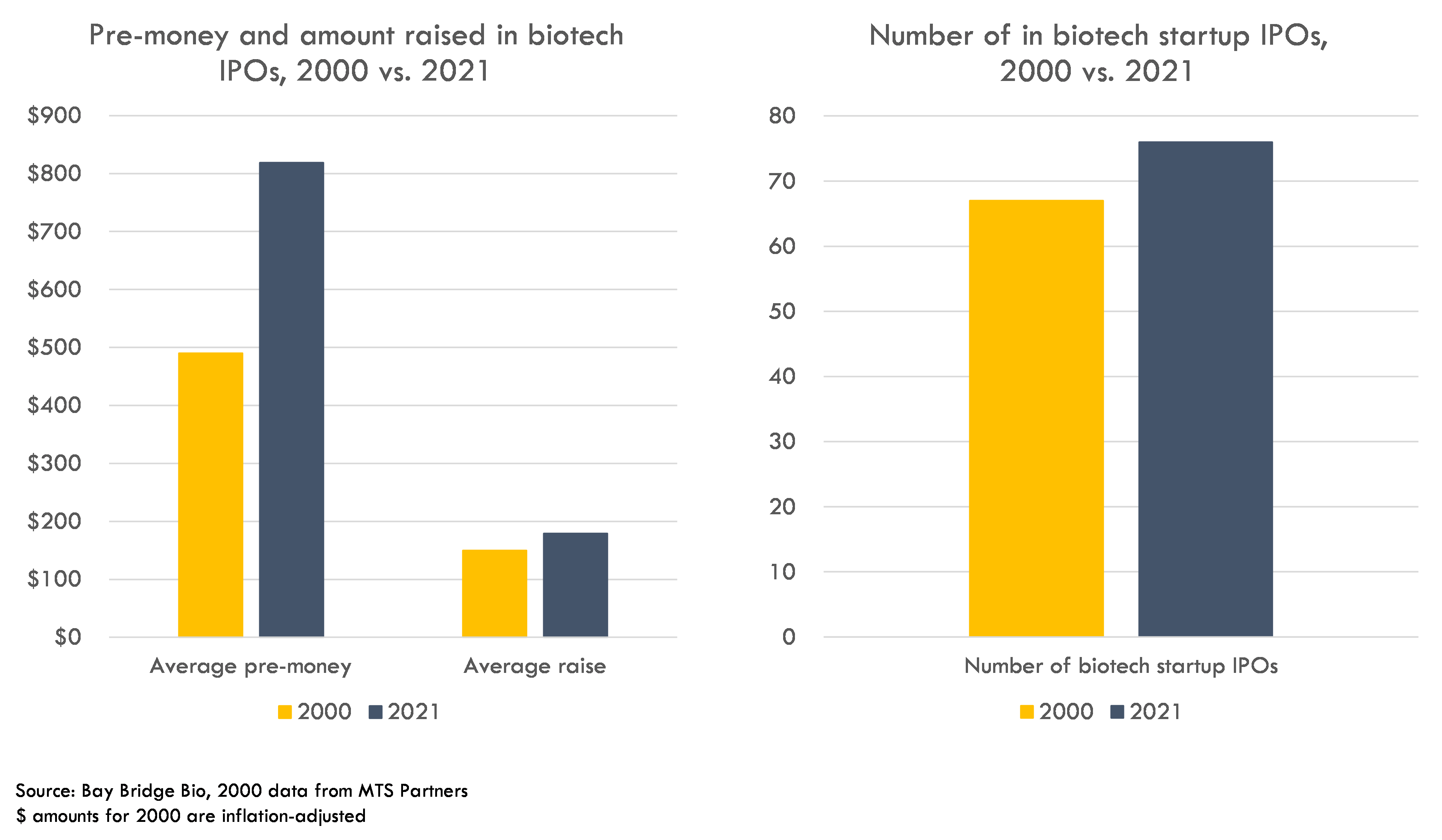

One can argue that the biotech market in 2021 was the most risk tolerant in the industry's history. The 76 biotech startup IPOs on US exchanges in 2021 is greater than the 67 biotech IPOs during the peak of the dotcom / genomics boom in 2000. The IPO classes of both 2000 and 2021 had a large number of preclinical IPOs, as well as IPOs of platform companies ranging from computational genomic medicine to cell therapy.

{kind=link}

The valuations of the biotech IPOs in 2021 were significantly higher than in 2000. In 2000, biopharma startup IPOs had an average pre-money of around $300M and an average raise of ~$90M. On an inflation adjusted basis, this is a pre-money of $490M and post-money of $640M. Compare this to the average IPO pre-money of over $800M in 2021.

While it is challenging to compare the market of 2000 to 2021 due to the number of changes that have occurred to the market and market structure, one can make a case that the 2021 market was more bullish than 2000. In that light, it isn't surprising (and is probably healthy) that the market has pulled back from 2021 levels.

Defensible clinical trial cost estimates

Get transparent cost estimates for any trial in minutes. Input an NCT ID or upload a protocol, then see a full cost analysis report.

Where is the bottom?

While the XBI is down 40% since its 2021 peak and the IPO market is at a standstill, venture funding has not yet slowed down and VCs are flush with cash, which provides support to the market. Interestingly, there has not yet been a traditional crash in the biotech market – the 40% year-over-year decline was slow and gradual, and broader indices like the S&P 500 and NASDAQ have performed well and are within 7% and 14% of their respective all-time highs.

We cannot know what will happen in the future, but we can analyze a range of scenarios and bound what might happen in the more likely scenarios. We will address this topic, and how companies and investors might prepare for various scenarios, in subsequent posts.