Top biotech venture capital funds of 2018-2023

by Richard Murphey

Updated April 28, 2023

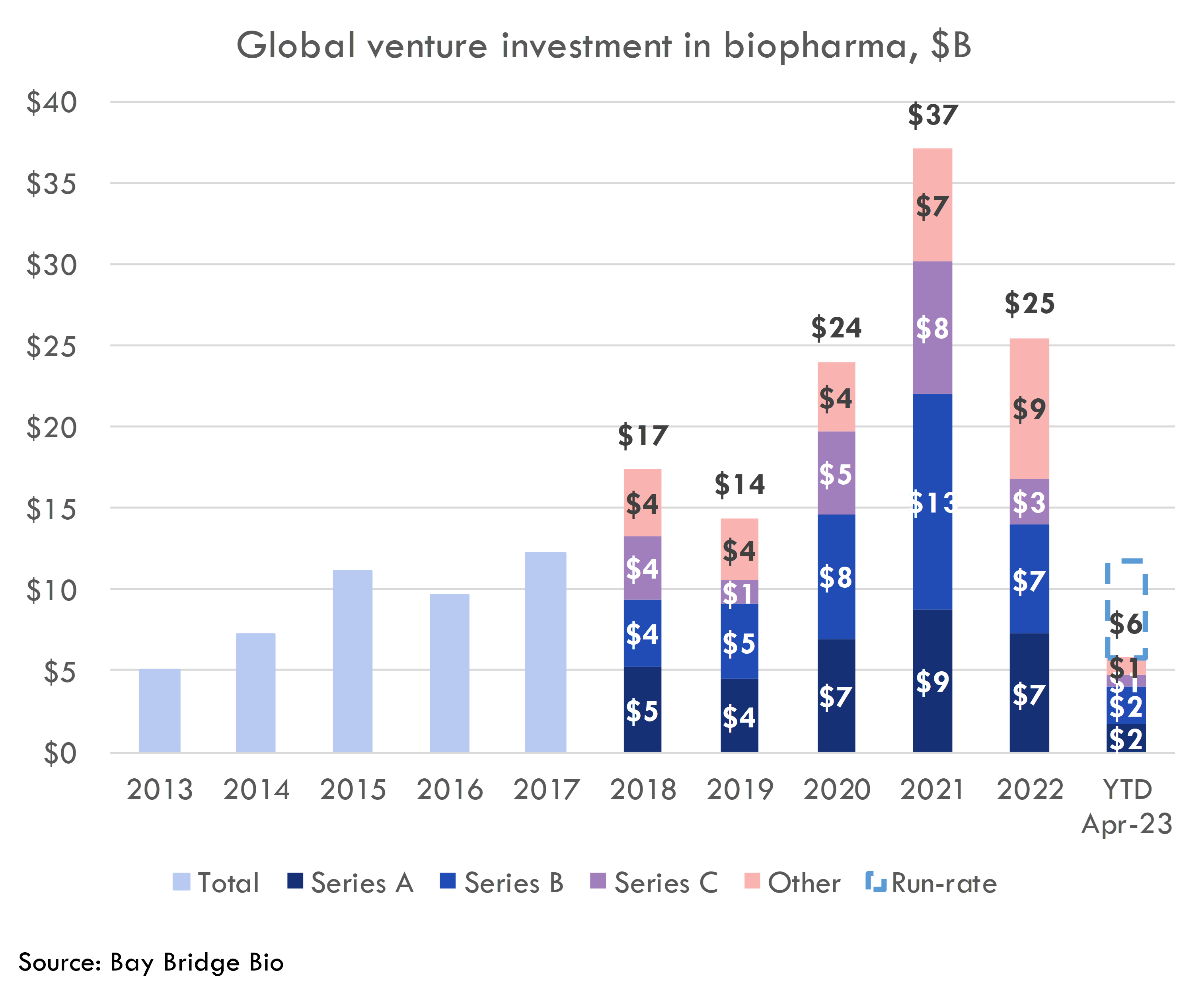

After a decade-long boom, biotech winter is here.

In 2023, venture capital investment into biopharma startups is on pace to hit its lowest level since 2016.

This post will describe the top biotech venture capital firms that drove this boom, and who is still investing today:

- What kinds of investors fund biotech startups?

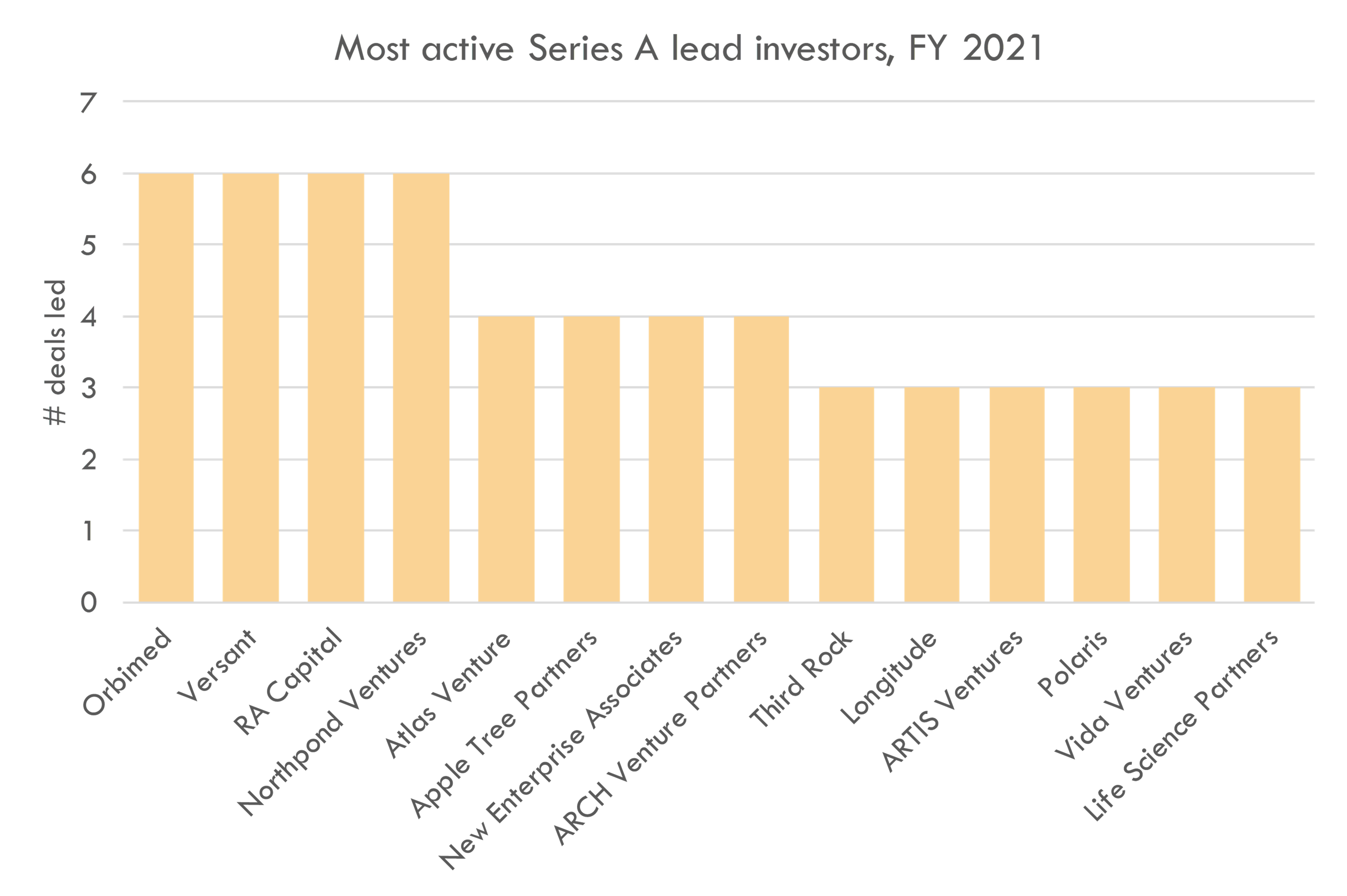

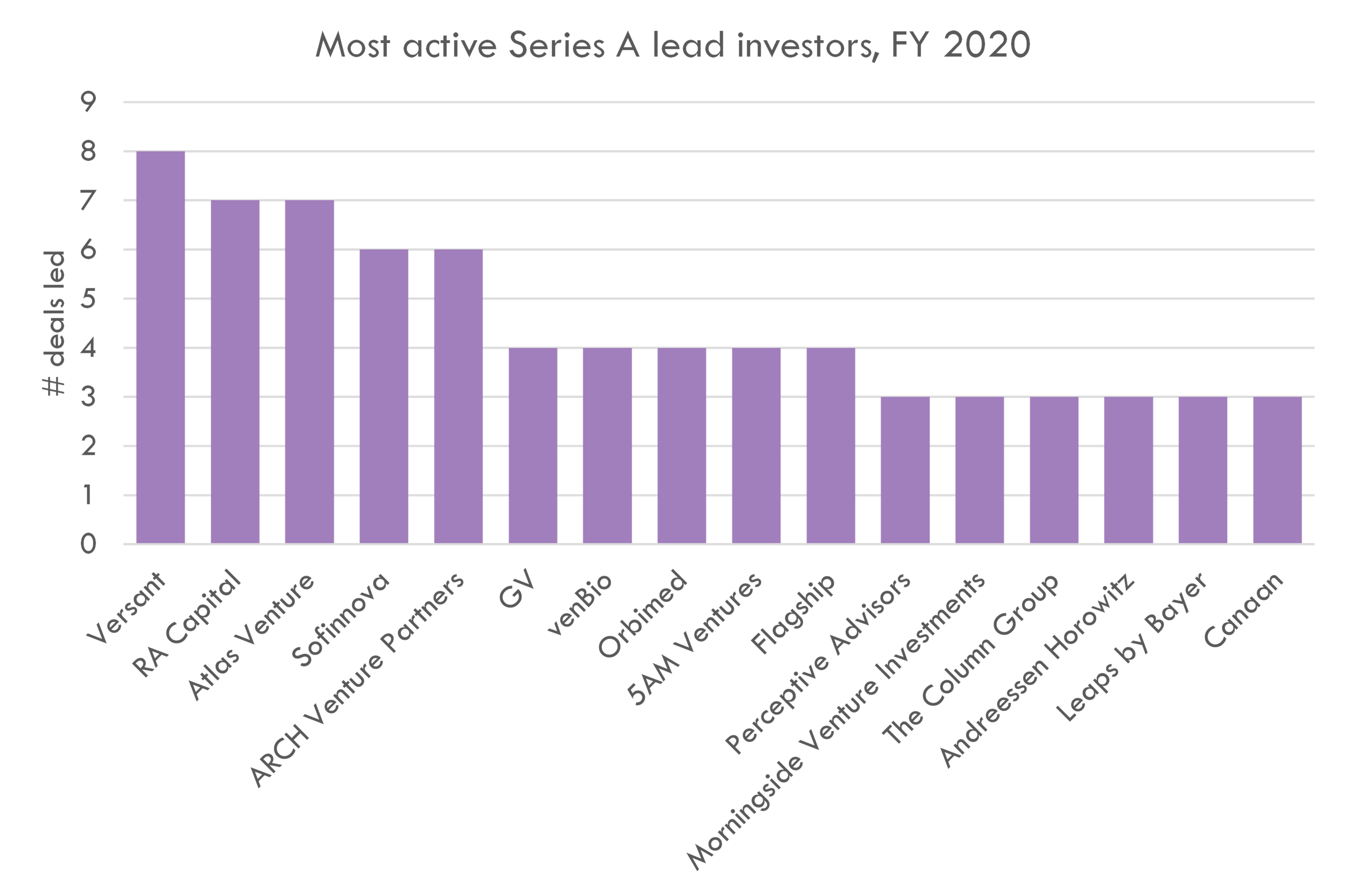

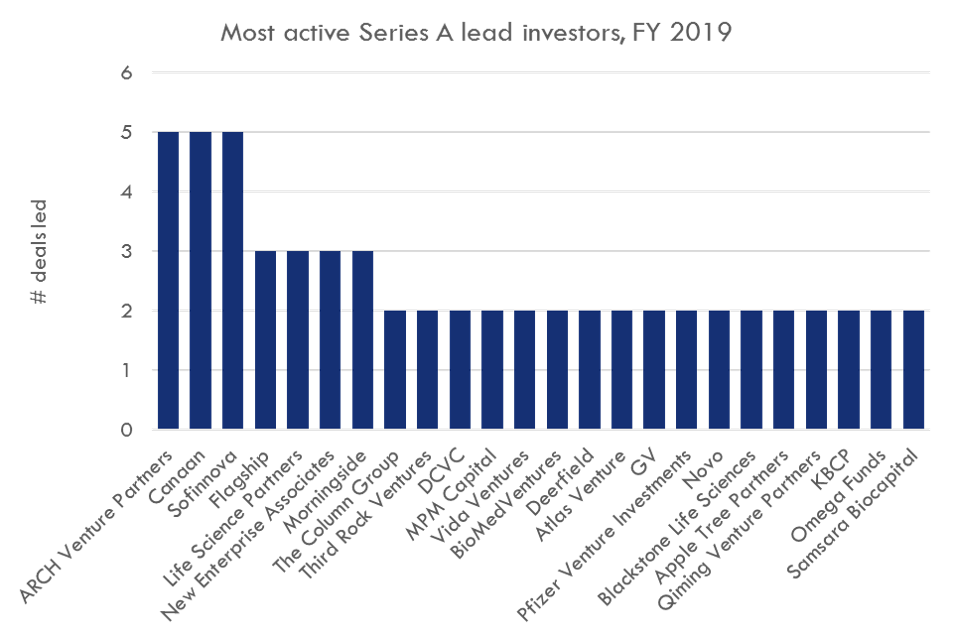

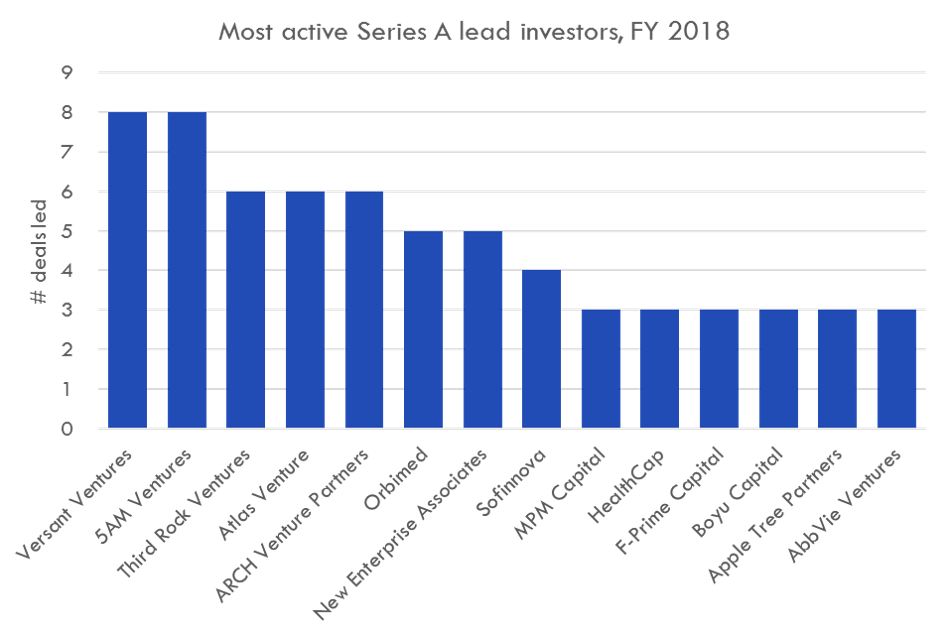

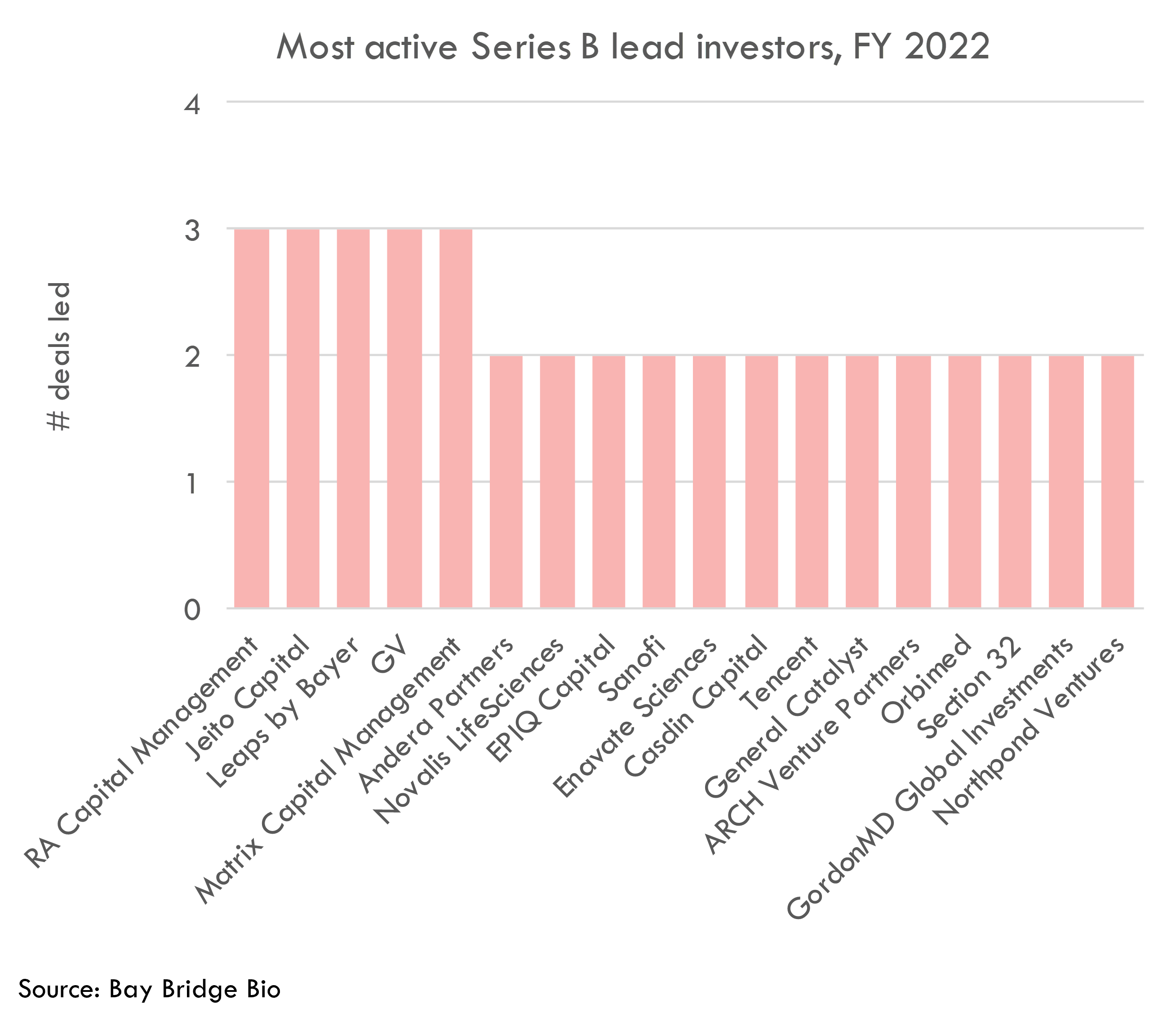

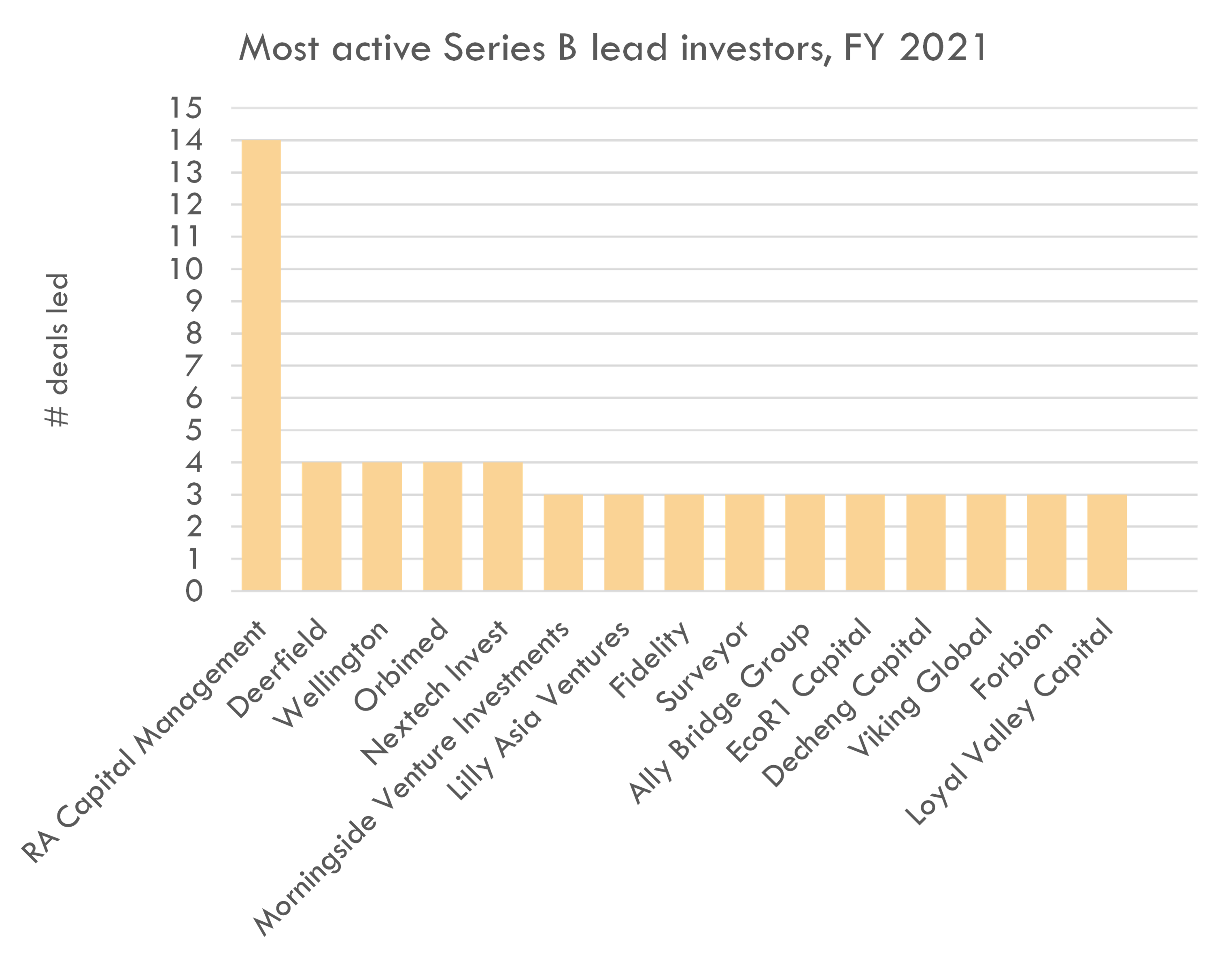

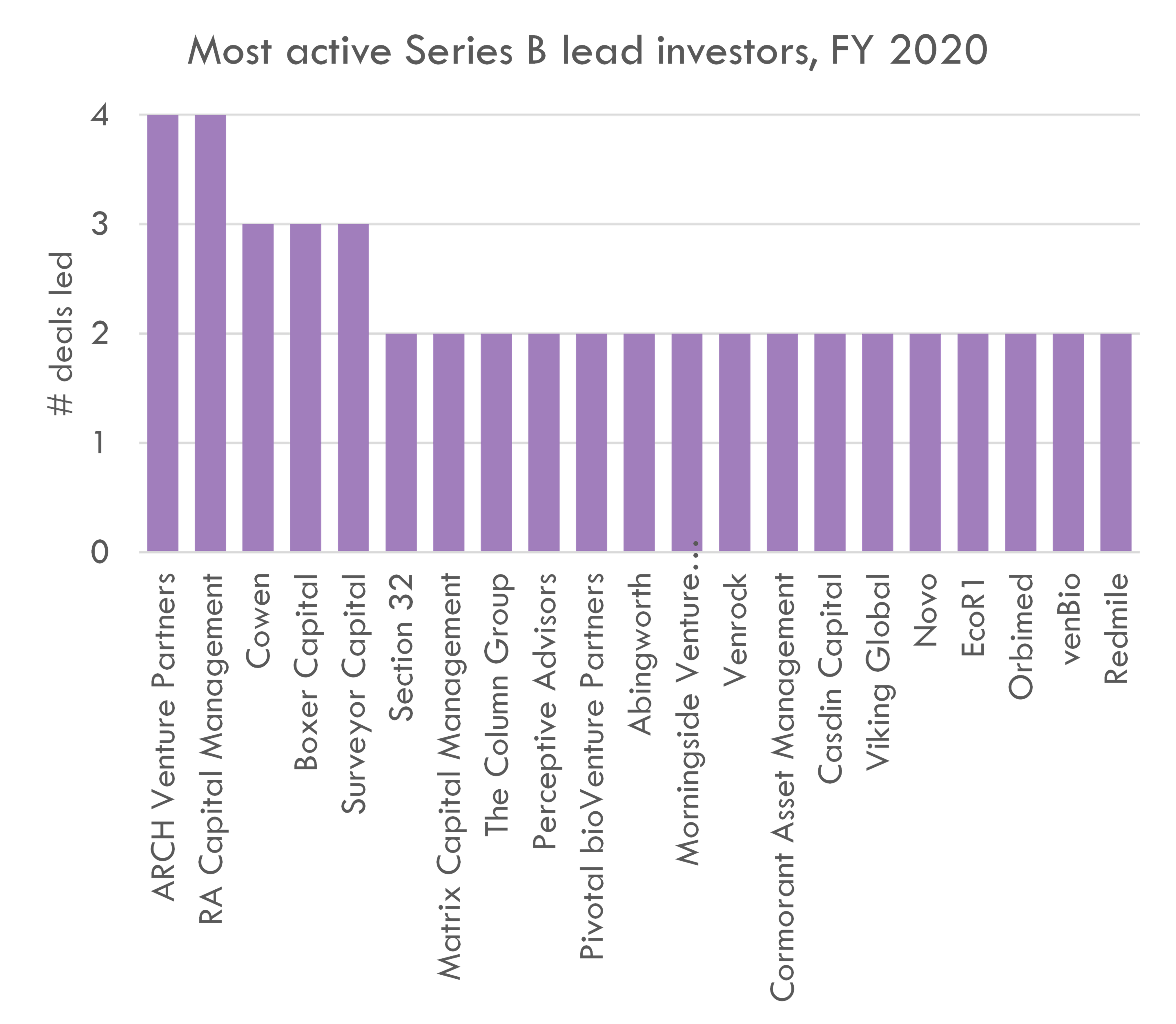

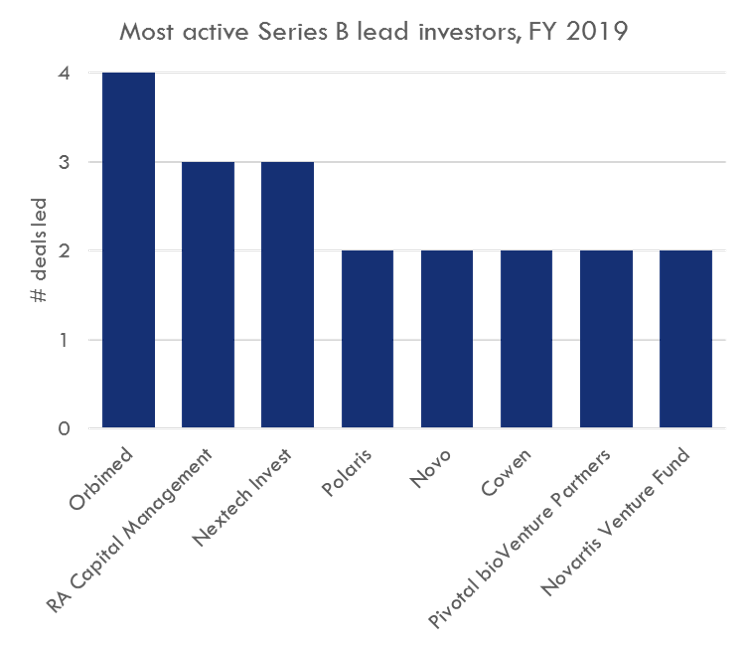

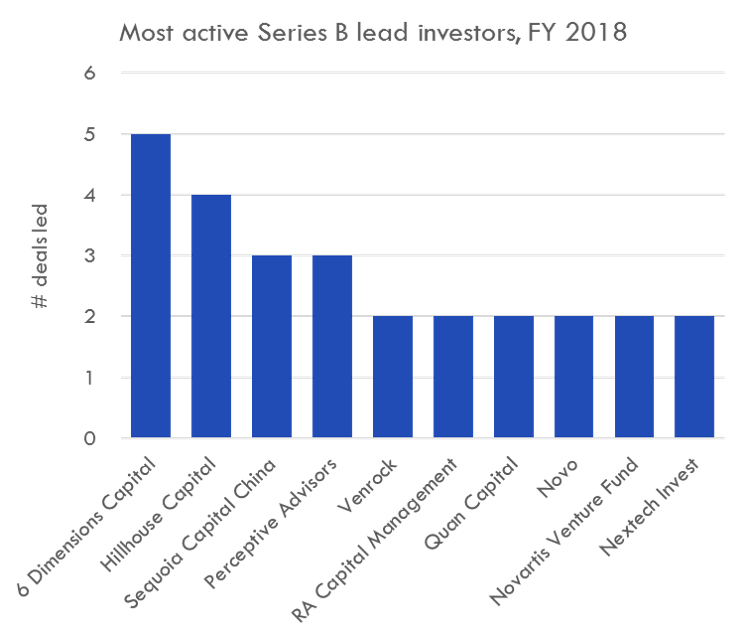

- Who are the most active biotech VCs in Series A and B rounds?

- Who are the most active seed and angel investors in biotech?

- Which VCs made the most money from exits in 2018 through May 2023?

Who's investing?

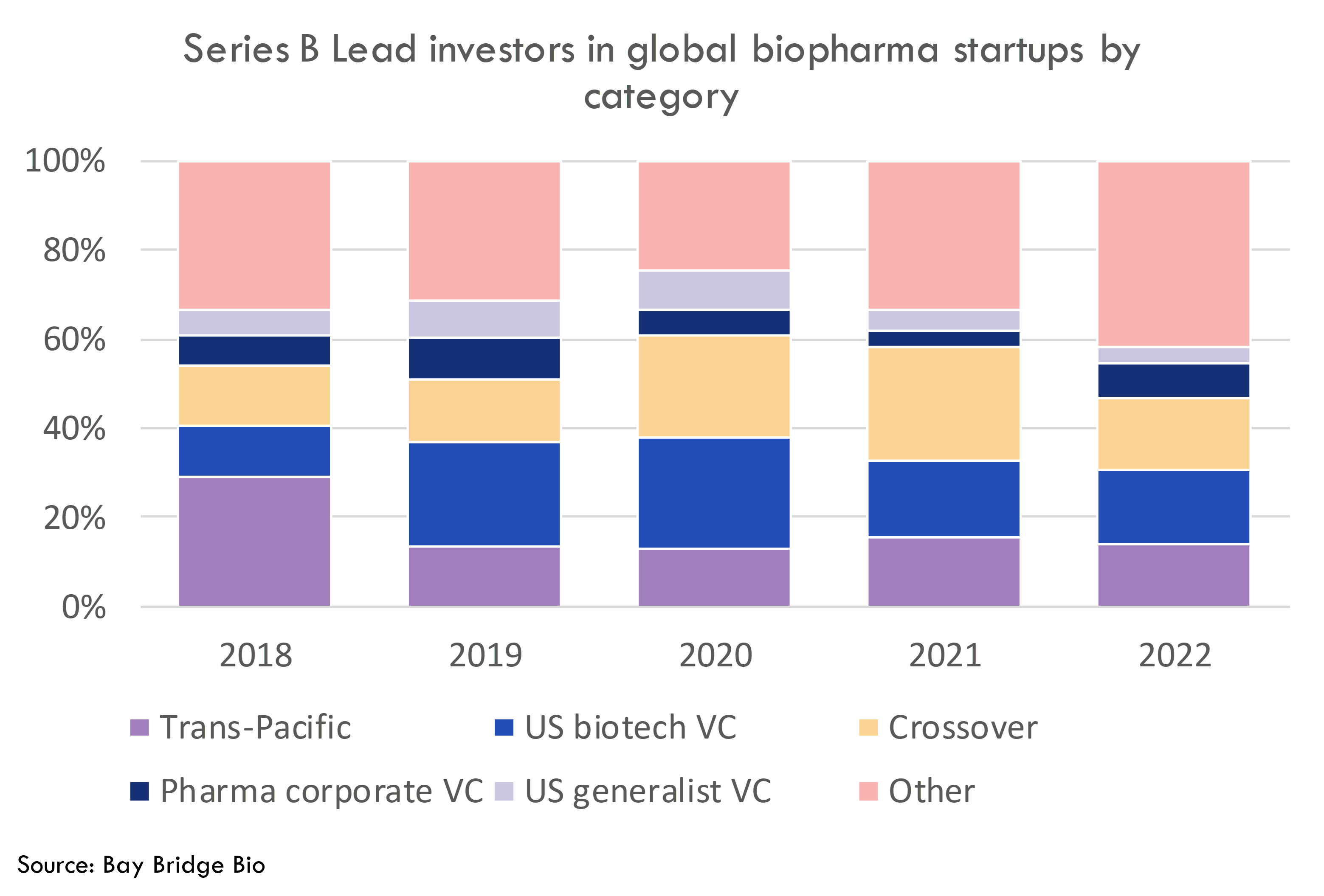

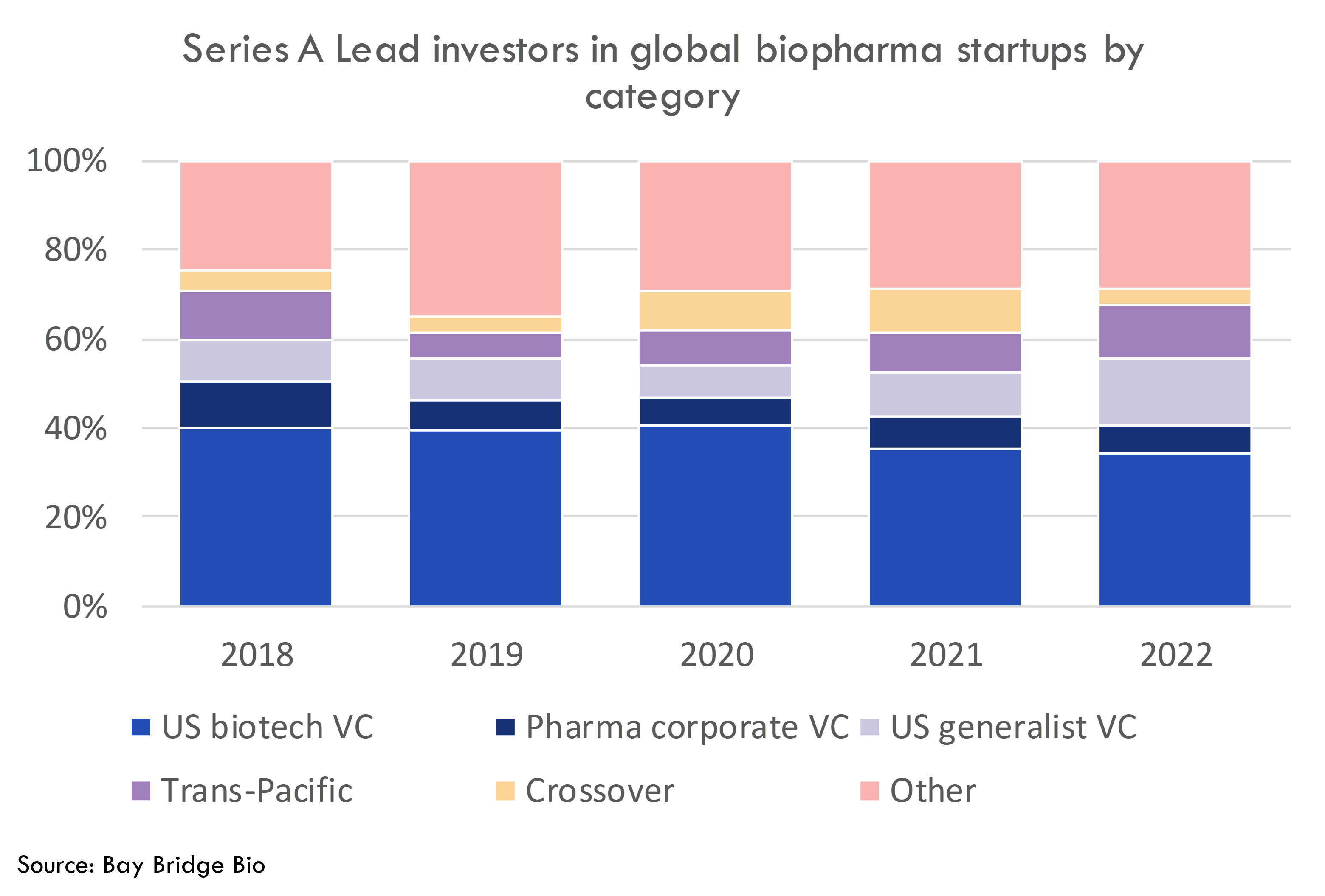

In 2021, it seemed like everyone was investing in biotech. Today, only a select few investors are still active. And they are doing fewer deals.

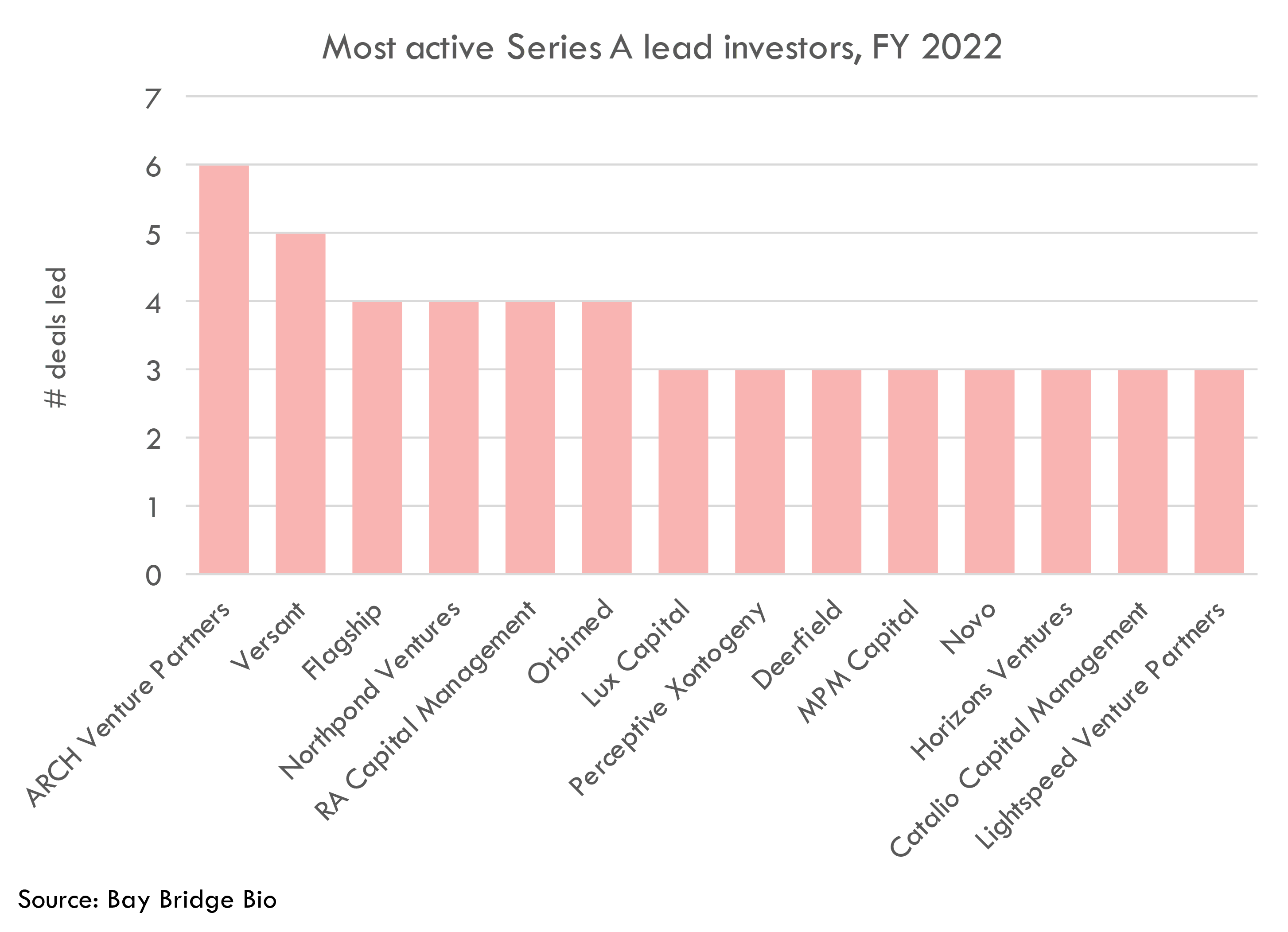

The established biotech investors -- venture and crossover funds like RA Capital, Orbimed, ARCH, and Versant -- are still active, but at a lower volume than in the past. In addition to the stalwarts, there is a new group of VCs that have been picking up the pace.

The below charts illustrate this trend. In 2022, we see a decrease in activity of crossover investors and established biotech VCs at the B stage, and an increase in "other" investors (including family offices, sovereign wealth funds, and European funds). At the Series A stage, etablished US biotech VCs are ceding share to generalist tech / techbio VCs.

Build defensible valuation models in minutes

Describe an asset or provide a ticker. Get a functional excel model with defensible assumptions. Stress-test assumptions, run scenarios, and do in-depth research, just by chatting with the agent.

A changing investor landscape

One paradox of venture capital investing today is that venture firms are still raising huge amounts of cash, despite investing less of that capital. Some of them, like ARCH, Flagship and Versant, are continuing to invest actively despite deteriorating downstream capital markets (these funds were some of the most active during the COVID bubble as well). Others are reserving more capital for their existing portfolio or to invest opportunistically. Other active investors at the Series A stage include techbio funds like Lux, Northpond and Lightspeed, and Catalio.

The crossover / Series B landscape has changed dramatically. RA Capital is still among the most active, though at a significantly lower level than in the past. Casdin and Orbimed are other traditional crossover funds that are still active (though at lower levels). Most of the other household crossover funds of years past have significantly scaled back.

Which VCs made the most from exits?

Below are the VCs who made the most from exits in 2018 through May 2023. This list includes biotech startups that raised $50M+ on NASDAQ or NYSE or were acquired while public (we don't have data for private M&A). The market values assume the investor held all shares since IPO. This table only includes data for companies where investors held 5% or more of common shares pre-IPO.

| Firm name | Num. of portfolio IPOs | Num. of portfolio public M&A | Proceeds at IPO price | Proceeds at May 3, 2023 | Portfolio IPOs | Portfolio public M&A |

|---|---|---|---|---|---|---|

| Flagship | 10 | 0 | $2,324,518,440 | $7,748,624,415 | Axcella Health, Evelo Biosciences, Kaleido Biosciences, Moderna, Rubius Therapeutics, Sigilon Therapeutics, Foghorn Therapeutics, Codiak Biosciences, Sana Biotechnology, Omega Therapeutics | |

| Orbimed | 37 | 9 | $2,523,243,319 | $2,093,371,200 | Alector, Armo Biosciences, Arcutis Biotherapeutics, Arvinas, Crinetics, 89Bio, Harpoon Therapeutics, Imara, Keros Therapeutics, LogicBio Therapeutics, NextCure, Passage Bio, Principia Biopharma, Prevail Therapeutics, Repare Therapeutics, SpringWorks Therapeutics, Tricida, Synthorx, resTORbio, Verrica Pharmaceuticals, Galecto, PMV Pharmaceuticals, Kinnate Biopharma, Graybug Vision, Silverback Therapeutics, Prelude Therapeutics, Fusion Pharmaceuticals, Terns Pharmaceuticals, Edgewise Therapeutics, Decibel Therapeutics, Oric Pharmaceuticals, Ikena Oncology, VectivBio, Janux Therapeutics, Adagio Therapeutics, Theseus Pharmaceuticals, Third Harmonic Bio | Armo Biosciences, LogicBio Therapeutics, Principia Biopharma, Prevail Therapeutics, Synthorx, Turning Point Therapeutics, Clementia Pharmaceuticals, Audentes Therapeutics, Loxo Oncology |

| Viking Global | 12 | 0 | $1,443,046,065 | $1,700,420,785 | BridgeBio, Moderna, Zentalis Pharmaceuticals, Athira Pharma, PMV Pharmaceuticals, 4D Molecular Therapeutics, Edgewise Therapeutics, Pharvaris, AbCellera, Talaris Therapeutics, Rallybio, Amylyx Pharmaceuticals | |

| PureTech | 3 | 0 | $319,561,897 | $1,643,537,926 | Karuna Pharmaceuticals, resTORbio, Vor Biopharma | |

| RA Capital Management | 38 | 5 | $1,405,022,140 | $1,143,880,077 | Akouos, Arvinas, Black Diamond Therapeutics, Crinetics, 89Bio, Imara, Lyra Therapeutics, Vaxcyte, Prevail Therapeutics, Solid Biosciences, Satsuma Pharmaceuticals, Synthorx, Olema Pharmaceuticals, Dyne Therapeutics, Kinnate Biopharma, Vor Biopharma, Bolt Biotherapeutics, iTeos Therapeutics, Inozyme, Connect Biopharma, Achilles Therapeutics, Day One Biopharmaceuticals, Werewolf Therapeutics, Janux Therapeutics, Acumen Pharmaceuticals, Aerovate Therapeutics, Cyteir Therapeutics, Icosavax, Adagio Therapeutics, Eliem Therapeutics, DICE Therapeutics, Tyra Bio, Pyxis Oncology, IO Biotech, LianBio, PepGen, AN2 Therapeutics, Acrivon Therapeutics | Akouos, Forma Therapeutics, Prevail Therapeutics, Synthorx, Ra Pharmaceuticals |

| ARCH Venture Partners | 15 | 1 | $1,607,373,751 | $983,409,265 | Beam Therapeutics, Homology Medicines, Gossamer Bio, Karuna Pharmaceuticals, Scholar Rock, Unity Biotechnology, Codiak Biosciences, Metacrine, Juno Therapeutics, Sana Biotechnology, Singular Genomic Systems, Erasca, Verve Therapeutics, Lyell Immunopharma, Prime Medicine | Juno Therapeutics |

| Atlas Venture | 16 | 1 | $1,358,004,698 | $850,301,545 | Akero Therapeutics, Avrobio, Bicycle Therapeutics, Generation Bio, Magenta Therapeutics, Replimune, Surface Oncology, Translate Bio, Unum Therapeutics, Dyne Therapeutics, Kymera Therapeutics, Ikena Oncology, Day One Biopharmaceuticals, Xilio Therapeutics, Vigil Neuroscience, Third Harmonic Bio | Translate Bio |

| Foresite Capital | 12 | 2 | $1,024,628,342 | $774,921,513 | Fulcrum Therapeutics, Keros Therapeutics, Arcus Biosciences, Replimune, Kinnate Biopharma, Aimmune Therapeutics, 10x Genomics, Pharvaris, Cullinan Oncology, Nurix Therapeutics, Lyell Immunopharma, Theseus Pharmaceuticals | Turning Point Therapeutics, Aimmune Therapeutics |

| Sofinnova | 16 | 7 | $515,171,525 | $770,769,196 | Akouos, Entasis Therapeutics, Galera Therapeutics, Hookipa Pharma, Iterum Therapeutics, Kiniksa Pharmaceuticals, Karuna Pharmaceuticals, NextCure, Principia Biopharma, Y-mAbs Therapeutics, Spark Therapeutics, Bolt Biotherapeutics, Inozyme, Vera Therapeutics, Aerovate Therapeutics, MaxCyte | Akouos, Entasis Therapeutics, Principia Biopharma, Audentes Therapeutics, Spark Therapeutics, Checkmate Pharmaceuticals, CinCor Pharma |

| Cormorant Asset Management | 22 | 5 | $457,214,791 | $757,836,431 | Avrobio, Constellation Pharmaceuticals, Kiniksa Pharmaceuticals, Kezar Life Sciences, Principia Biopharma, Avidity Biosciences, Satsuma Pharmaceuticals, C4 Therapeutics, Olema Pharmaceuticals, Atea Pharmaceuticals, Tarsus Pharmaceuticals, Galecto, Design Therapeutics, Longboard Pharmaceuticals, Rain Therapeutics, Biomea Fusion, Aerovate Therapeutics, Erasca, Ambrx, Monte Rosa Therapeutics, Elevation Oncology, Immuneering Corporation | Constellation Pharmaceuticals, Forma Therapeutics, Principia Biopharma, Turning Point Therapeutics, Prometheus Biosciences |

| Perceptive Advisors | 16 | 2 | $901,081,550 | $748,678,265 | Crinetics, Frequency Therapeutics, Ideaya Biosciences, Kodiak Sciences, Lyra Therapeutics, MeiraGTx, Solid Biosciences, SpringWorks Therapeutics, Verrica Pharmaceuticals, Athira Pharma, C4 Therapeutics, Rain Therapeutics, Pyxis Oncology, IsoPlexis, LianBio, Acrivon Therapeutics | Dova Pharmaceuticals, Prometheus Biosciences |

| Third Rock | 9 | 2 | $1,028,995,856 | $679,413,004 | Constellation Pharmaceuticals, Fulcrum Therapeutics, Magenta Therapeutics, Neon Therapeutics, Pliant Therapeutics, Revolution Medicines, Decibel Therapeutics, Relay Therapeutics, Nurix Therapeutics | Constellation Pharmaceuticals, MyoKardia |

| Versant | 15 | 3 | $1,282,224,916 | $657,222,166 | Akero Therapeutics, Aprea Therapeutics, Black Diamond Therapeutics, Crinetics, Gritstone Oncology, Oyster Point Pharma, Passage Bio, Repare Therapeutics, Aligos Therapeutics, Pandion Therapeutics, Lava Therapeutics, VectivBio, Monte Rosa Therapeutics, Century Therapeutics, Graphite Bio | Oyster Point Pharma, Audentes Therapeutics, Pandion Therapeutics |

| Venrock | 8 | 2 | $676,870,870 | $634,447,614 | Constellation Pharmaceuticals, Kiniksa Pharmaceuticals, Milestone Pharmaceuticals, Unity Biotechnology, AveXis, 10x Genomics, Instil Bio, Cyteir Therapeutics | Constellation Pharmaceuticals, AveXis |

| Baker Brothers | 13 | 3 | $822,026,420 | $612,711,506 | Atreca, Cabaletta Bio, Hookipa Pharma, IGM Biosciences, Kiniksa Pharmaceuticals, Kodiak Sciences, Principia Biopharma, Prelude Therapeutics, Aligos Therapeutics, Spark Therapeutics, Immunocore, Achilles Therapeutics, TScan Therapeutics | Forma Therapeutics, Principia Biopharma, Spark Therapeutics |

Build defensible valuation models in minutes

Describe an asset or provide a ticker. Get a functional excel model with defensible assumptions. Stress-test assumptions, run scenarios, and do in-depth research, just by chatting with the agent.

Top seed funds

Prior to 2018 or so, there wasn't really a biotech seed market. But in the last few years, the biotech seed market has exploded. Dozens of new investors have emerged who are focused on funding scientifically ambitious biotech companies, often started by younger scientific founders (as opposed to the experienced professional entrepreneurs that often run VC-backed biotech startups).

Data on seed funding is less comprehensive than later-stage funding, as these companies don't publicize their raises as often. To identify the top biotech seed investors, I asked biotech founders in my network who have raised $1M+ in seed capital in the last 2 years.

This methodology ensures that the investors on the list are 1) actively investing and 2) founder friendly. However, this list is not comprehensive and certainly omits some great investors. If you are a founder and think I should add an investor to the list, let me know.

Note: this list was created in 2020-2021. These investors may or may not be active as of 2023

| Fund name | Blog | Notable investments | Location | Investor type | Team | |

|---|---|---|---|---|---|---|

| 5AM Ventures | https://5amventures.com/news/ | Achaogen, Arvinas, Ceterix Orthopedics, Vor Biopharma, Viveve | Boston, San Francisco Bay Area | Seed, Venture | Kush Parmar, Andrew Schwab, David Allison, Jamil Beg, Mira Chaurushiya, Brian Daniels, Rebecca Lucia, Deborah Palestrant, John Diekman, Michelle Ho, Pengpeng Li, Kevin Nguyen, Scott Rocklage, Jason Ruth | |

| 8VC | https://8vc.com/resources/blog/ | Color Genomics, Bolt Threads, Mantra Bio | San Francisco Bay Area | Seed, Venture | Francisco Gimenez, David Moskowitz, Alex Kolicich | |

| Alix Ventures | https://www.alix.vc/content-1 | Sling Health, Circularis, Xilis, Elegan | San Francisco Bay Area | Seed | Chas Pulido, Ron Shigeta | |

| Andreessen Horowitz | https://a16z.com/posts/ | Octant Bio, Scribe Therapeutics, Asimov, Freenome | San Francisco Bay Area | Seed, Venture, Growth | Judy Savitskaya, Jorge Conde, Vijay Pande, Andy Tran, Frank Chen, Julie Yoo, Justin Larkin, JT Evans | |

| Apollo Health Ventures | https://medium.com/apollo-ventures-insights | Hamburg | Accelerator, Seed | Jens Eckstein, Nils Regge, Alexandra Bause, Anela Vukoja | ||

| Apollo | San Francisco Bay Area | Accelerator | Max Altman, Sam Altman, Jack Altman | |||

| ARTIS | https://www.av.co/insights | Stemcentrx, Freenome, Eko, IdbyDNA, Fabric Genomics, Aether Biomachines | Seed | Stuart Peterson, Vasudev Bailey, Austin Walne | ||

| Asset Management Ventures | https://assetman.com/perspectives-health-care/ | Evidation, Freenome, HealthTap, Audentes Therapeutics, 3T Biosciences | San Francisco Bay Area | Seed, Venture | Skip Fleshman, Lou Lange, Rich Simoni, Melina Mathur, Luke Lee | |

| Augustin Ku | Cloud9, Hexagon bio, StemCentRx, SyntheX | Las Vegas, Nevada | Angel | Augustin Ku | ||

| Axial | https://axial.substack.com/ | Culture Biosciences, Inflammatix, Genedit, Unnatural Products | San Francisco Bay Area | Angel | Joshua Elkington | |

| BioRock Ventures | https://angel.co/mary-wheeler/syndicate?utm_campaign=syndicate_direct_link | Vaxcyte, Seal Rock Therapeutics, Octagon Therapeutics, AN2 Therapeutics, Primmune Therapeutics | San Francisco Bay Area | Seed | Mary Wheeler | |

| Bioverge | https://medium.com/@Bioverge | Notable Labs, Enclear Therapies, Echo, Blue Mesa, Occamz Razor | San Francisco Bay Area | Angel | Neil Littman | |

| Boom Capital | Mammoth Biosciences, A-Alpha Bio, FaunaBio, System1 Biosciences | San Francisco Bay Area | Seed | Celestine Schnugg | ||

| Cambrian Biopharma | New York City | Seed | James Peyer, Christian Angermeyer, Juliete Han, Tauhid Ali, Dennis Yamashita, Georg Terstappen | |||

| Canaan | https://www.canaan.com/latest | Arrakis Therapeutics, Synthekine, Onkos Surgical, Pathios Therapeutics, Pact Pharma | San Francisco Bay Area, New York City | Seed, Venture | Brent Ahrens, Colleen Cuffaro, Julie Grant, Nina Kjellson, Stephen Bloch, Tim Shannon, Wende Hutton | |

| Civilization Ventures | BillionToOne, Omada Health, Lemonaid, Foresight Diagnostics, Singular Bio, Convergent Genomics, Rocket Pharma, Prellis Biologics | San Francisco Bay Area | Seed, Venture | Shahram Seyedin-Noor | ||

| Codon Capital | Arcus Biosciences, Bolt Threads, Flexus Biosciences, Oric Pharmaceuticals, Shattuck Labs, Zymergen | San Francisco Bay Area | Seed, Venture | Karl Handelsman, Mitchell Mutz | ||

| DCVC | https://www.dcvc.com/news.html | Agenovir, C16 Biosciences, Cofactor Genomics, Orca Bio | Seed, Venture | Zachary Bogue, John Hamer, Kiersten Stead, James Hardiman, Armen vidian, Ali Tamaseb, Anna Fokina, John Cumbers, Christopher Meldrum, Andy May | ||

| Digitalis Ventures | https://digitalisventures.com/notes/ | Good Therapeutics, Terray Therapeutics, The Mighty, MollyBox, Onc.AI, Rejuvenate Bio | New York City, Los Angeles, San Francisco Bay Area, Boston | Seed | Geoff Smith, Sam Bjork | |

| E-Fund / Point Reyes Management | 1910 Genetics, Industrial Microbes, Spiral Genetics, Nano Cheq | San Francisco Bay Area | Seed | Sophia Collier, Chula Reynolds, Matt Esh | ||

| Endpoint Ventures (angel syndicate of founders of GeneWEAVE and Endpoint Health) | Billion to One, Shasqi, Indee Labs, Meru Health, Reverie Labs, The One Healthcare Company, Viosera Therapeutics, Synkrino | San Francisco Bay Area | Angel | Diego Rey, Jason Springs, Leo Teixeira | ||

| Fifty Years VC | https://fiftyyears.substack.com | HelixNano, Opentrons, Tierra Biosciences, Athelas, Memphis Meats | San Francisco Bay Area | Seed | Ela Madej, Seth Bannon, Shuo Yang | |

| Foobar VC | Circularis, VitroLabs, Radix Labs, Nextmind, HelixNano | Seed | David Helgason | |||

| FoundersX Ventures | 1910 Genetics, Menten.ai, Kernal Bio, Trexo Robotics | San Francisco Bay Area | Seed to Growth | Helen Liang, Benjamin Xu, Tom Kosnik, Cyrus Hodes, John Sun, Wendy Hayes | ||

| Genoa Ventures | https://www.genoavc.com/news | Adarza Biosystems, Intabio, Intervenn, Ionpath, Synthomics, Tropic Biosciences | San Francisco Bay Area | Seed | Jenny Rooke, Richard Kenny, Bill Hyun, Paul Conley, Paco Cifuentes | |

| Georges Harik | 23andMe, uBiome, Metabiota, Adimab, Tegmine Therapeutics | San Francisco Bay Area | Seed | Georges Harik | ||

| Gwen Cheni | Tinctorium, Lupa Bio, Synthex | San Francisco Bay Area | Angel | Gwen Cheni | ||

| Hof Capital | https://medium.com/hof-capital | Insitro, Metagenomi, XGenomes, Ovid Research, BillionToOne | New York City, San Francisco Bay Area, London | Seed, Venture | Victor Wang, Hisham Elhaddad, Neil Devani | |

| Humboldt Fund | Memphis Meats, Meatable, NotCo, Mission Barns, Ansa Biotechnologies, Geltor, Miroculus, Finch Therapeutics, BrightSeed | San Francisco Bay Area | Seed | Benjamin Quiroga, Sebastian Bernales | ||

| Hummingbird Ventures | BillionToOne, Basecamp Research, Kernal | London, Antwerp | Seed, Series A, Series B | Firat Ileri, Tess van Stekelenburg, Pablo Lubroth | ||

| Incube Ventures | Corhythm, Neurolink, Rani Therapeutics, Spinal Modulation | San Jose | Seed | Mar Perez, Andrew Farquharson, Mir Imran, Talat Imran, Mark Sieczkarek, Wayne Roe | ||

| IndieBio | https://indiebio.co/blog/ | New Age Meats, SugarLogix, Prellis Biologics, Jungla | San Francisco Bay Area, New York City | Accelerator | Jun Axup, Po Bronson, Stephen Chambers, Rodrigo Mallo Leiva, Alex Kopelyan, Pae U | |

| James Hong | Athelas, Hexagon Bio, Tegmine Therapeutics, Emerald Cloud Lab, Emerald Therapeutics | San Francisco Bay Area | Angel | James Hong | ||

| Jude Gomila | http://www.judegomila.com/ | Circle Pharma, Cofactor Genomics, Coral Genomics, Viosera Therapeutics, Gingko Bioworks | San Francisco Bay Area | Angel | Jude Gomila | |

| KdT Ventures | https://medium.com/@kdtventures | Tierra Biosciences, PathAI, 54Gene, Elegan | Austin | Seed, Venture | Cain McClary, Mack Healy, Rima Chakrabarti, Phil Grayeski | |

| Khosla Ventures | https://www.khoslaventures.com/blog/all | Arpeggio Bio, BIOAGE, Cellino, E25Bio, Editas Medicine, eGenesis, Eligo Biosciences, Encellin, Fountain Therapeutics, GEn1E | San Francisco Bay Area | Seed, Venture | Vinod Khosla, Alex Morgan, Justin Kao, Kristina Simmons | |

| Liquid2 Ventures | C16 Biosciences, Solugen, Athelas | San Francisco Bay Area | Seed | Michael Ma, Nate Montana, Joe Montana, Mike Miller | ||

| Longevity Fund | https://ldeming.posthaven.com/ | Alix Oncology, Celevity, Decibel Therapeutics, Fauna Bio, Precision Biosciences | San Francisco Bay Area | Seed, Accelerator | Laura Deming | |

| Luminous Ventures | Oxford VR, Optellum, Vital, Active Global, Astroscreen, Biobeats, Beyond…, Climax Foods, Ellipsis Health, Facesoft, Flox | London | Seed | Isabel Fox, Lomax Ward, Simon Hsu, Peter Crane, Alasdair Thong, Miao He, Josh Liu, John Spindler, James Joll, Csaba Konkoly | ||

| Lux Capital | https://luxcapital.com/news/ | Halo Neuroscience, Recursion Pharma, Genocea, Auris Surgical Robotics, Kallyope | New York City, San Francisco Bay Area | Seed | Zavain Dar, Adam Goulburn, Ian Peikon, Robert Paull | |

| Mars Bio | https://www.marsbio.vc/media | Minicircle, Better Earth, Encellin, Armada | Seed, Venture | Robert Rhinehart, Arye Lipman, Llewellyn Cox, | ||

| Mayfield | https://www.mayfield.com/news/ | Mission Bio, Mammoth Biosciences, Qventus, Endpoint Health | San Francisco Bay Area | Seed, Venture | Tim Chang, Arvind Gupta, Ursheet Parikh, Navin Chaddha | |

| Mission BioCapital | Zymergen, Cell Design Labs, Alector, Bolt Threads, Nocion Therapeutics, Wild Type, Pandion Therapeutics, Glycomine | San Francisco Bay Area | Seed, Venture | Doug Crawford, Peter Parker, Steve Tregay, Johannes Fruehauf, Eric Linsley, Robert Blazej | ||

| New Ventures Funds (Scientia Ventures) | https://www.scientiavc.com/news | ADC Therapeutics, Royalty Pharma, Fibrogen, Cibus | New York City | Seed, Venture | Jonathan Finn, Mark Finn, Henry Glorikian, Rory Riggs, Richard Warburg, John Dessouki | |

| NFX | https://www.nfx.com/ | Mammoth Biosciences, C2i Genomics, Twist Biosciences. Armada, Genome Compiler | San Francisco Bay Area, Israel | Seed | James Currier, Pete Flint, Gigi Levy-Weiss, Morgan Beller, Shayma Sharif, Brittany Yoon | |

| Nordic Makers | https://www.nordicmakers.vc/best-practice/#sub-page-1 | Nextmind, Helix Nano, Biolib | Nordic Countries | Seed | Moaffak Ahmed, Michael Seifert, Esben Gadsboll, Klaus Nyengaard, Martin Von Haller Gronbaek, Lars Floe Nielsen, Alexander Aghassipour, David Helgason, Benjamin Ratz | |

| OMX Ventures | Finch Therapeutics | Seed, Venture | Daniel Fero, Nick Haft, Craig Asher | |||

| Pacific 8 | http://www.pac8.com/news | Mammoth Bioscience, BillionToOne, Dorian Therapeutics, Fauna Bio, Karius, Cura Therapeutics | Taipei, San Francisco Bay Area | Seed | Chris Shu, Jack Liang, Ser-Chen Fu | |

| Paul Buchheit | http://paulbuchheit.blogspot.com/ | Cofactor Genomics, Bikanta, Cue Health, Comprehend, Luminist | San Francisco Bay Area | Angel | Paul Buchheit | |

| Paul Graham | http://www.paulgraham.com/ | Angel | Paul Graham | |||

| Petri Bio | Boston | Accelerator, Seed | Tony Kulesa, Jaye Goldstein, Brian Baynes, Jamie Goldstein, Christian Caraco, Josh Moser | |||

| Point Nine | https://medium.com/point-nine-news | Berlin | Seed | Louis Coppey, Ricardo Sequerra, Christoph Janz, Pawel Chudzinski | ||

| Presight Capital | Terran Biosciences, Peptilogics, Enclear Therapies | New York City | Seed | Christian Angermayer, Fabian Hansen | ||

| Refactor Capital | https://medium.com/refactor | Synthetic Biology, Computational Biology / Chemistry, Therapeutics, Longevity, Genomics, AI / ML, Other | San Francisco Bay Area | Seed | Zal Bilimoria, David Lee | |

| Sam Altman | https://blog.samaltman.com/ | Angel | Sam Altman | |||

| Sea Lane | Cradle Genomics, Spring Discovery, Q Bio | Seed, Venture | Ling Wong | |||

| Tech.Bio | San Francisco Bay Area | Seed | Omri Drory | |||

| True Ventures | https://trueventures.com/blog | Membio, Fauna Bio, Intervenn Biosciences, Prellis Biologics, Symbiome | San Francisco Bay Area | Seed | Rohit Sharma, Adam D'Augelli | |

| Tsingyuan Ventures | https://medium.com/tsingyuan-ventures | Spotlight Therapeutics, Namocell, Erisyon, Cardea Bio | Seed | Michael Jin, Steve Sun, Biao He | ||

| Wireframe Ventures | Mammoth Biosciences, Reverie Labs, Geneticure | San Francisco Bay Area | Seed | Harsh Patel, Paul Straub | ||

| Y Combinator | https://blog.ycombinator.com/ | Viosera Therapeutics, Gingko Bioworks, Alpine Roads, Solugen, Athelas | San Francisco | Accelerator | Jared Friedman, Paul Bucheit, Michael Seibel, Uri Lopatin | |

| Yleana Venture Partners/Emles Advisors | Seed |

To stay updated on biopharma startup funding and exit trends through 2020, check out our free startup dashboard for summary info updated on a regular basis.

You may also like...

List of recently funded biotech startups

Valuations of biotech startups from Series A to IPO

Bay Bridge Bio Startup Database

How to value biotech companies

Did you enjoy this article?

Then consider joining our mailing list. I periodically publish data-driven articles on the biotech startup and VC world.